[#28] Why has the 30% market share cap on UPI volumes been extended?

Is there a glass ceiling as a new UPI App?

I read an article this week about how NPCI, to break the UPI market concentration within the top 3-4 apps, had originally capped the market share at 30%, taking December 2020 as a deadline. This deadline was then extended to Dec 2022, and now and now they’ve come out and extended that deadline by 2 years, till the end of 2024. You can check out the article here. The Top 10 apps control 98% of the volume of UPI transactions. And this is very heavily skewed towards the Top 3, which control 92% as of April ‘24. (PhonePe 51%, Gpay 35%, Paytm 6%).

So this deadline will probably have to be extended again, because if the focus is organic shifting of volumes, then there is still a long way to go.

But then why are there so many UPI Apps operating, if the top 3 collectively have > 90% market share? Over the last 12 months, there were 65 - 70 UPI Apps processing volumes on UPI. Even if we go down the list, we see Whatsapp (#13 in terms of volumes processed, 2815 Cr / month) Jupiter (#21, 710 Cr / month), Slice (#24, 608 Cr / month), Fampay (#25, 588 Cr / month), Navi (#32, 317 Cr / month), Flipkart UPI (#36, 174 Cr / month), Go Niyo, (#60, 16.7 Cr / month), MMT (#60, 19.3 Cr / month), Fave (#69, 1.16 Cr / month) & Cheq (#70, 1.13 Cr / month).

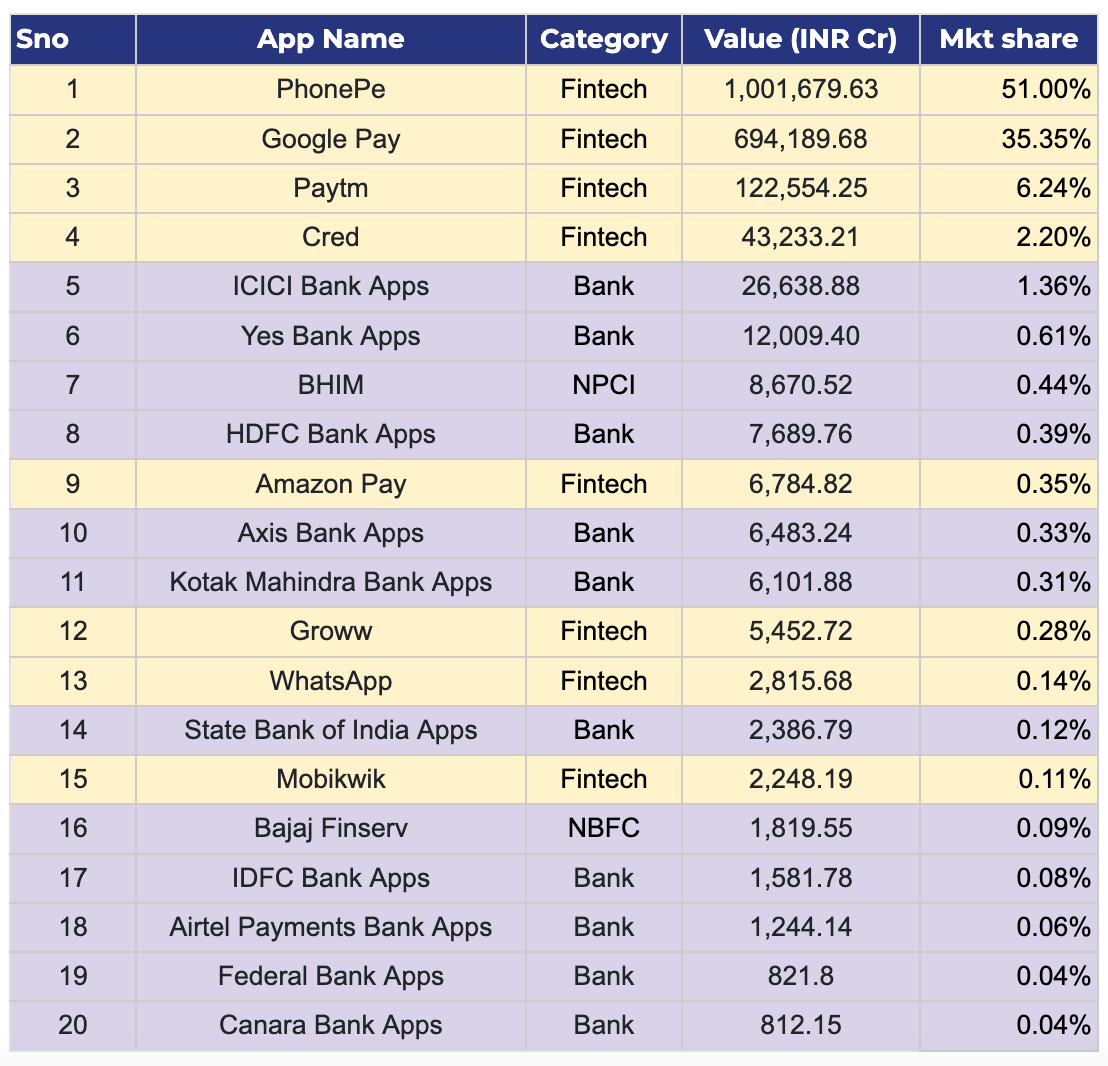

Let’s take a look at the data from April ‘24.

Consumer facing companies are backward integrating into UPI to acquire customers for their core business

Out of the total INR 19 Lac Crore, or $240B of UPI volumes in April ‘24, majority are concentrated in the Top 4, which are all fintechs. (PhonePe, Gpay, Paytm & Cred)

In terms of volumes even though ICICI, Yes, BHIM, and HDFC are collectively contributing to ~3% market share, in absolute terms, this equates to ~55k Cr worth of volumes through UPI every month. That’s $6B volumes coming through UPI every month. And close to 25 - 35M transactions coming in per month. So while we talk about PhonePe having the highest market share, and tend not to pay attention to other banks and their UPI apps, the UPI numbers coming through banks are not insignificant

And that’s probably why consumer facing applications: AmazonPay (#9, 6000 Cr), Groww (#12, 5452 Cr) are getting into this space. Even a fraction of the market can mean significant volumes - the logic of the bigger TAM, and less market share required to have a sustainable business. Of course, in the case of UPI, with limitations of pricing, sustainability is a question, which is why a lot of these apps cross sell a lot of other products

If the projections are true, and UPI will power 90% of digital payments by 2028, then these apps are playing the long game right now. There may not be clarity on what will happen to pricing, but it’s a race for market share & customer acquisition right now. The Indian digital payments market is projected to hit $400B by 2028. Even 0.01% of this market is ~300 Cr.

And that’s probably why there is backward integration into UPI. Newer apps: Jupiter, Navi, FamPay etc, who’s core operations lie in something else: be it neo-banking, loans, or even travel. They have a business model, what they need is customers, and that’s what they will get from UPI. And that’s probably why ABFL launched their own ABCD App for the end customer: they have a vision to acquire 30M within the next 3 years

Consumer Apps still seem to be used only for app specific transactions, and not all UPI payments

Based on the average value per transaction data, the way I see UPI apps evolve is the following:

I’ve assumed that since the majority of the market share of UPI payments lies with PhonePe, GooglePay and Paytm, the average general UPI transaction has an AoV of ~1-1.5k.

According to reports, Amazon AoV for non-prime users is 1 - 1.2k, which is in-line with the average transaction value on AmazonPay. And players like Go Niyo & MMT, which are travel focused, have an AoV of 4k - 6k, which is probably due to the higher ticket size of folks either traveling, or investing. Groww: which is primarily for investing into stocks and mutual funds as an AoV on its UPI of INR 6799. And volumes seem to tell the same story: Groww UPI in Dec ‘23 had a market share in UPI volumes of 0.22%. This spiked to ~2x to 0.35% in Jan ‘24, probably due to the january effect in the markets, and then dropped back down to 0.16%

But what is interesting is that despite Flipkarts AoV in India being 1k - 2k, the AoV on Flipkart UPI is much lower at ~ Rs 500. So while sure, flipkart orders are being paid for through flipkart UPI, there are other, lower ticket size orders that are being paid through Flipkart UPI. And even Navi, a platform that gives out loans, has an average ticket size of Rs 266. So I’d assume transactions of a lower ticket size, such as bill payments perhaps are what these platforms are being used for. And the bill payments strategy probably feeds into the overall strategy of customer acquisition for core business.

While there is no change at the top of the table (UPI Apps by volume of transactions), there are changes below.

Data from April ‘23 - ‘24

Huge chasm between most & least preferred UPI Apps: Top 6 App positions in terms of volume processed remain unchanged despite 2 showing degrowth: Paytm, Gpay, Paytm, CRED, ICICI, Yes & BHIM all remain in the same positions → top 6 apps in terms of UPI volumes processed. And this is despite the fact that Paytm, Yes Bank & BHIM have grown slower than the market: Paytm & Yes volumes have actually shown degrowth from April ‘23 to ‘24 of 21% and 3% respectively. BHIM has grown by 17% but that is less than half of the market growth of 37%.

Fintech Apps in the Top 20 have shown > 100% growth: CRED, Groww, Mobikwik & Whatsapp have grown faster than the market.

CRED has grown by ~100%, from volumes of 20k Cr in April ‘23 to 43k Cr in April ‘24.

Whatsapp: Has grown by 113% to ~2815 Cr

Mobikwik: Has grown by 143% to 2248 Cr, which is promising for its IPO plans

Groww has grown the most: From 80 Cr in April ‘23 to 5452 Cr in April ‘24, a growth of ~6715%!

But even though their market share & volumes have grown, they’re all at < 5% of the market. In fact, except for CRED, which is 2.20% market share in April ‘24, of the total 19 L Cr UPI volumes processed, most are sub 0.5%.

So then how will this play out?

1. Opportunity for 1-2 fintechs to step up as a challenger for UPI volumes: NPCI will continue to shift deadlines unless there are other fintechs / banks who are able to step up and divert more volumes. PhonePe, Gpay & Paytm have a monopoly on UPI volumes. But CRED caters to a very specific audience: only those who have credit cards, so it may be unlikely that they will scale to > 5% of UPI volumes. And after Paytm Payments bank went down, it may be some time before customers make their way back to Paytm: some have probably switched already (like me) and gone to Gpay / PhonePe as their primary UPI App of choice. Of course, willingness to spend to get the share of mind of the customer is still a big question.

2. Backward integration into UPI for customer acquisition: Customer facing Merchants / Ecomm players (scaled up) with established business models will continue to build their own UPI Apps in the hope of acquiring more customers for their core business. This makes the most sense for players who already have products they can monetize such as marketplaces (Amazon, Flipkart), Investments (Groww), Loans (Navi), Travel (MMT, Niyo). And especially enabling things such as bill payments will encourage customers to come back to the app, and then enable the app to cross sell products

3. Top heavy skew, with a long tail of UPI Apps: There may not be enough incentives for players to scale up UPI volumes through their app after a certain point. Up to a certain extent - sure. For customer acquisition, and ability to cross sell, yes. But beyond that, it’s pretty hard to compete with the brands in the market. PhonePe’s 50% market share in UPI is no joke. And to be able to break the PhonePe, Gpay, Paytm monopoly would require brand marketing campaigns in the hundreds of Crores. And especially after the last two years, where start-up focus has moved back to profitability from growth, it’s unlikely many will be willing to make that commitment. And also, even 1% of a currently $240B and projected to be $400B in 2028 is $40B in volumes. Assuming a 1% market share of $400B, and UPI transaction per day through the app, at an AoV of Rs 2000 this is a base of ~5M loyal customers. Even to get here would require a tremendous expense.

Let’s look at CRED. In FY22 it spent INR 976 Cr on marketing. In FY23 it spent 713 Cr. In April ‘23 its UPI share was 1.45%, which is now at 2.20%.

4. The fintech who makes UPI payment most convenient will win: Customers use UPI because it is convenient. And they use PhonePe, Gpay because it is now a habit to simply take out phones, and scan & pay for offline, or online, and in the case of mobile checkout, redirect the customer to the app. To make UPI payments even more convenient, there will have to be innovations on 1) reducing the need for mobile devices to make a payment: this is sometime in the future, but some sort of biometric solution for ID verification and payment and 2) Entire experience of the payment should be in-app: By removing the need for redirection, and making the entire UPI payment experience in app.

Are there any network effects in UPI? I can't see any? The heavy concentration of market shares in the hands of the top two players seems odd. How do you explain it?