[#42] The Klarna IPO & LazyPay pause: What does the future of BNPL look like?

There have been a bunch of news coming out this last week on different BNPL players, both based in India and globally. Klarna, the blue-eyed BNPL of Europe, and Sweden, second only to Revolut, the global neobank, is apparently filing for an IPO in New York in early 2025.

Compared to global equivalents, the valuation, revenues, and revenue multiples that others are currently, or in the past at, Klarna definitely seems like it is undervalued. It has close to 150M users, as compared to its closes public market equivalent Affirm, which has 19.5M users. And there’s another reason I think this: It’s because Klarna has a European banking license, so it should actually be valued at revenue multiples that global neobanks are being valued at, especially since its started roll out its bank account product in August 2024.

You can also checkout the piece I wrote about neobanks, which could very well be where Klarna is headed.

![[#40] The case for neobanks in India: what can we learn from global successes such as Nubank?](https://substackcdn.com/image/fetch/$s_!G8yT!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F3d81c4d2-68c0-4341-8025-90f2bcf45e1e_1600x896.png)

But in India, the BNPL landscape is not as cheery, and while global equivalents have IPO’ed they are all loss making

And on the other hand, in India, the news is not as great. Lazypay, which is a BNPL method powered by its parent company: PayU (Prosus) had to temporarily pause its operations because RBI identified some issues with its KYC process. And in the past few years, as the Digital Lending Guidelines have come out, BNPL in India has been languishing: NBFCs unwilling to take risk without FLDG (First Loss Default Guarantee). As a result of this, BNPL in India, as a standalone product, or even as a fintech that has an in-house NBFC is struggling. And there’s another reason for this: RBI to crack down on unsecured lending had introduced risk weights, mandating that if an NBFC wants to lend out 100%, then they have to have 125% raised, to cover their potential losses.

And as a result of new regulations, BNPL in India has gone through change:

Zestmoney, once hitting ~300-400 Cr of GMV per month tried to be sold to PhonePe. When that fell through, it was sold in a fire sale to DMI Finance, which in October 2024 was banned by RBI to give out any more loans.

Hit revenues of ~$26M in FY23, and Amazon already has an 8% stake. Reportedly getting closer to Amazon buying them out at a $150-$175M price point.

Struggling with customer acquisition (has ~6M if reports are to be believed), and earlier in FY24, had to let go of ~100 employees to manage monthly cash burn. They also operate a bit in the grey area, with regards to lending: They don’t have a NBFC or a bank partner, but instead lend on their books through a a $1B credit line given to them by Franklin Templeton, Finuvo LLC and Catalina Finance

Globally also, things don’t look so great.

While Affirm and Klarna still seem to be doing well (well being a relative term), Zip ended operations from multiple regions in FY23. Afterpay, which was acquired by block in 2021 has had mounting bad debt losses. Openpay went defunct. Slice, which started out as card issuer, never really recovered after the RBI circular that prevented PPI wallets being funded by credit lines, and then the DLG, and has now merged with North East SFB. Reportedly Tabby, the BNPL based out of Saudi is profitable, but there are no public numbers, so it’s hard to verify.

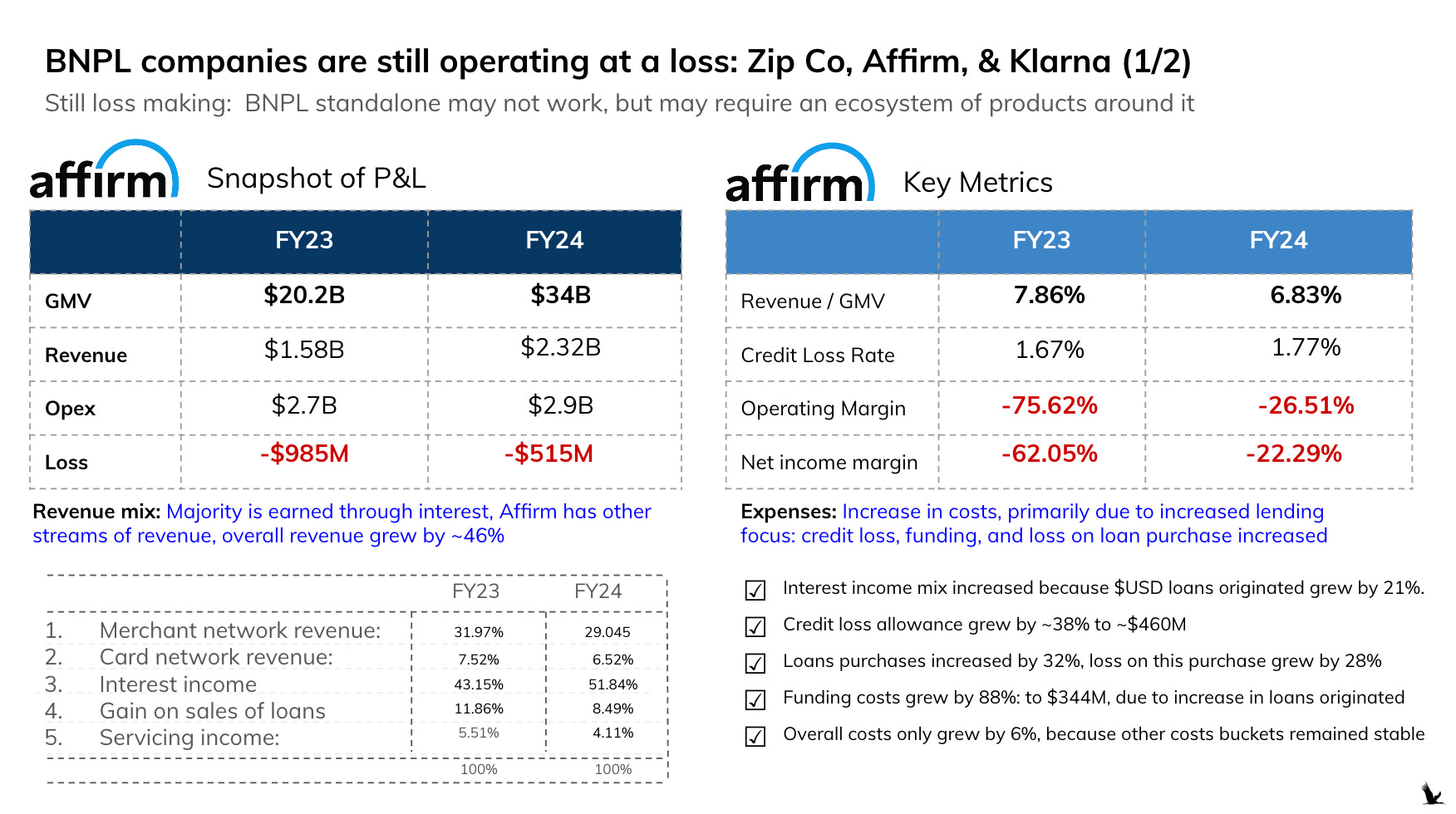

And despite the “success” of Klarna and Affirm: The fact is, 10+ years post founding, both these companies are still operating at a loss.

Affirm was founded in 2014, and IPO’ed in 2021. in FY24, it made a loss of $515M! Now granted, this has reduced, from the close to $1B of losses in FY23, but one would expect better of a company that’s been around for this long.

It’s costs over the last 2 years have been stable, its revenues have gone up because its booked more loans: 21% more in terms of USD to be exact. And lending, while lucrative, has a bunch of costs attached to it: bad debt, credit loss allowances, and funding costs. What’s heartening is that this isn’t the only revenue Affirm makes: while interest income is still the biggest chunk: close to 50%, it also makes a significant portion through MDR & fixed fees charged to merchants (3-6% MDR, and $0.3 fixed fee per transaction).

But here’s the concerning part: non lending costs don’t seem to be getting optimized

Sure, with lending, maybe there is no room to optimize costs. But what about the rest of it? In terms of processing payments: these are the following revenue buckets, and costs buckets

Transaction processing revenue buckets:

Total growth of both line items together: ~31% YoY

Merchant network revenue: FY23 → $507M, FY24→ $674M

Card network revenue: FY23 → $119M, FY24: → $151M

Transaction processing cost bucket:

Total growth ~33% YoY

Processing costs FY23 → $257M, FY24→ $343M

The cost of processing transactions seem be broadly growing at the same rate. So as Affirm processes more and more transactions, the cost of this will grow linearly, putting the pressure to lend more, book more loans, and boost the interest income. That is never a good place to be in.

Here is where Klarna is in slightly better shape. If we annualize its H1 results, it is booking ~2.5x more GMV than Affirm, which is probably because it’s present in 45 regions, as compared to Affirm, which is in US, Canada, and now rolling out in the UK. Affirm’s entry into Europe, and UK probably signals the start of it applying for its own banking license as well.

Klarna’s losses are less, and seem to present a path to profitability: in FY24 it was profitable at an operating margin level, and annualized, stands to lose ~$50M in FY24, not a small amount, but not as large as a $500M loss either!

2 things that Klarna seems to be doing better than Affirm:

It’s transaction processing costs seem much more optimized when compared to revenue growth → its able to drive revenues, while keeping costs down

Transaction processing & servicing cost: H1 23 → $244.17M, H1 24 → $266.04M. Grew by 9% from H1 FY23 to H1 FY24

Transaction processing revenue: H1 FY23 → $779.85M H1 FY24 → $1,012.05M

Grew by ~30%.

Majority of its revenues actually come from transaction and service revenue, not interest and late fees

To me, this is really interesting, because it signifies adoption of Klarna as a method, and as a way to pay, not just use for BNPL. On Klarna you can link other methods, such as your Mastercard and VISA, and pay those, instead of using Klarna’s “Pay in 4” method.

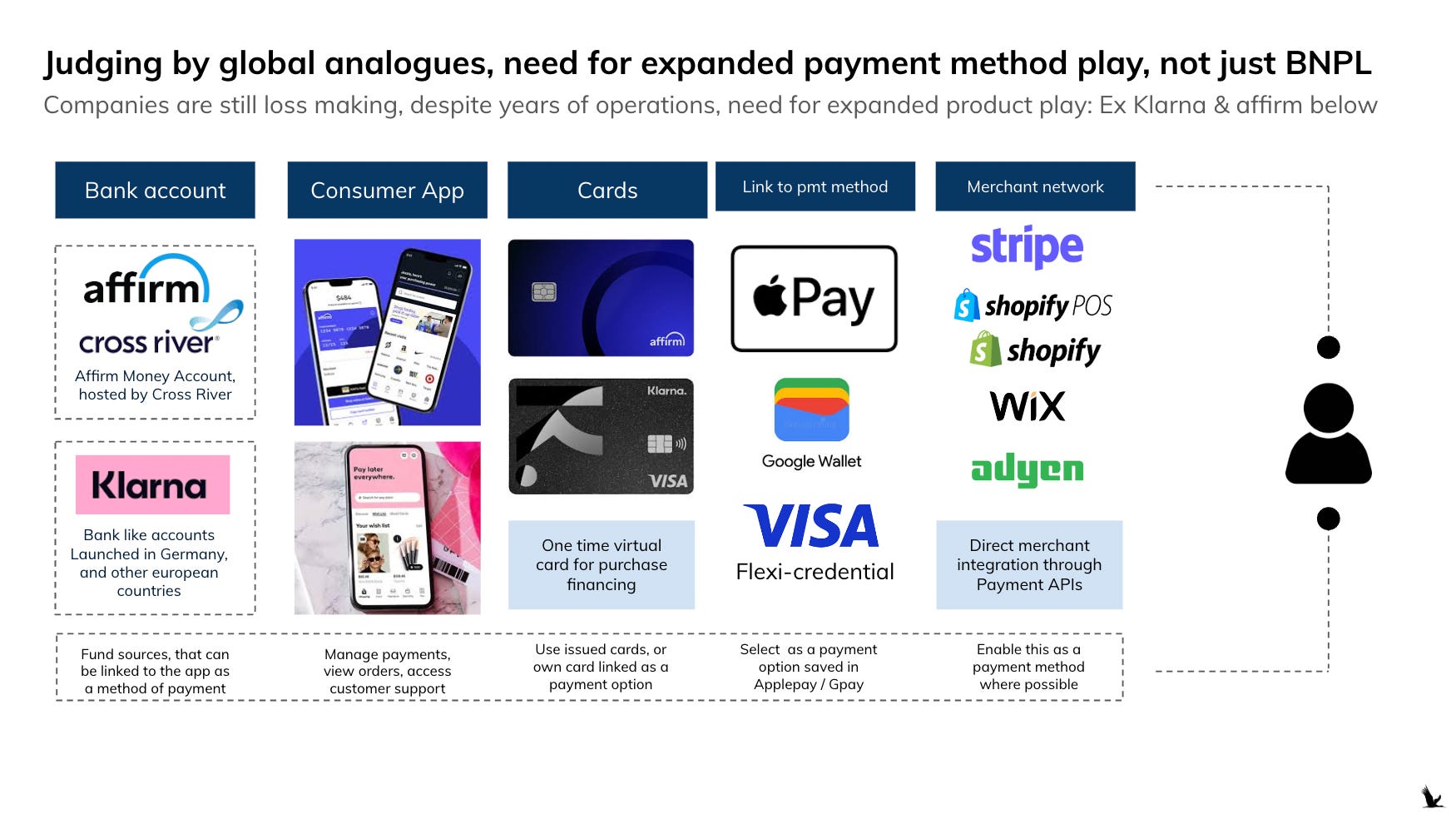

What is clear: BNPL is important, and drives value, but as a standalone play, it doesn’t work:

As a product, the interest bearing BNPL method will majorly be used by those individuals who may need this product more than others, and were unable to get it through other sources. The users using this for convenience will stop using it once charges are tacked on. And thus, unless you’re a bank, like Nubank for example: or you have other products: such as Klarna as a payment method, not just BNPL, life can get very hard.

Multiple products are paramount, to create an ecosystem, where different products can be used for different needed. And there also has to be ease of use: As payments move to mobile apps, and are driven by ApplePay, Google Wallet, and your UPI apps in India, it becomes super important to get the distribution play sorted, and see what other add on products can be built, that support paying through this as a method.

Usually what I’ve seen BNPL apps do, is acquire the user, and then try to “cross-sell” stuff to them, which are usually interest bearing loans, with a fervour that borders on harassment. Maybe that worked in the past, but it definitely doesn’t work anymore.

Klarna & Affirm both seem to be expanding their products & features to support easier usage as a payment option: Bank Accounts, which can then be linked to their consumer app, or a 3rd party app such as Applepay, or GoogleWallet. Consumer Apps, that allow easy shopping, payment, and rewards accrual inside the app. Co-branded cards, for ease of payment, and acceptance both across online and offline merchant networks.

They’re also aggressively going after partnerships: VISA Flexi Credential & Affirm, and how both have recently partnered with Googlewallet and Applepay, to link them as a method of choice on their apps.

But for BNPL, and payment methods to win: ease of set-up, checkout visibility, and linking to mobile apps at the time of set-up is key

Every customer has atleast 2-3 methods of payment now. Usually there’s your savings account based payment, through a debit card, or through real time payment rails, such as UPI. Then you have your credit cards, which are still primarily through Mastercard & VISA. And then there could be co-branded, specific rewards cards, and maybe a BNPL method that is preferred. And all of these usually are already saved on the merchants you shop at, and / or on your preferred mobile app.

So, when you want to use BNPL, or a new method, or set this up, what KEY is the partnerships with merchants and apps, and linking these methods to preferred payment apps. It’s not enough to just show this as an option at checkout, and expect the customer to go through multiple hops to pay, when there is an easier, more convenient option already saved.

Hey Ambika, great read! Very informative. Are the slides just to supplement the post, or do they form a part of a bigger read/report?