[#40] The case for neobanks in India: what can we learn from global successes such as Nubank?

Neobanks hold the potential to not just redefine retail banking, but the entire lending & payments landscape

Traditional banks are slow to innovate. This is a fact. And they’re slow with good reason: in the world of fintechs, with constant innovation, speed, and shipping products, sometimes it may be good to have an institution that moves slowly, and with temperance, especially since they’re the backbone of the financial industry.

But how slow is too slow? According to an article in the Financial Brand, three quarters of customers say that they would spend more money with a company that can provide a good digital customer experience. Most banks are still in very early stages of this, and this is easy to tell: just compare the experience you have in a traditional bank app / portal, versus a new age fintech app: such as Cred, or PhonePe. In fact, I would argue that fintechs exist because banks are slow at innovation.

UPI is a good example: banks were slow to adopt, but fintechs took it up, and drove usage & customer experience

UPI is a great example: It’s the 3rd party apps such as PhonePe, Paytm, and Gpay that are really responsible for UPI taking off in India. Banks were hesitant to adopt this new innovation, and were not able to provide the same convenience that fintechs apps provide. It’s only now that UPI has become a key part of the Indian consumer’s life that banks are investing in their own UPI Apps, and experiences.

Globally, it seems like people have caught on. And to solve the experience & innovation layer, neobanks seem to be how banking is evolving, because traditional banks are simply too slow to keep up with the pace of innovation in the fintech world.

And if you take a look at global neobanks, some of which have gone public, they’re not all just fancy packaging, and customer experience. The metrics around not just users, but also revenue and profitability show the sustainability of neobanks as a business model. Its also the fact that it’s not just targeting the unbanked or underbanked, but also getting users who already have a bank account: its able to offer more convenience, and better products at greater speed.

And with the way the fintech landscape in India is structured, with banks being the powerhouse, there is a need for a new age type of bank, which is less conservative, and quicker to innovate

Nubank, Revolut, and Kakaobank, due to favourable regulations have all been able to acquire banking licenses in their respective areas of operation. Their revenue and profitability metrics show promise: This is not just a “fancy app” that is driving MAU / DAU metrics. Its also able to generate revenues and profits consistently.

Let’s take Nubank as an example, and examine some of the metrics further:

I had done a deep dive into Nubank’s Q1 FY24 (Jan - March ‘24) report. You can check it out below:

![[#31] Nubank: Decoding user growth of the LATAM neobank amidst credit disbursals](https://substackcdn.com/image/fetch/$s_!ytJL!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F6149417c-9bd6-44a1-b18b-d85b1ce4b59b_1366x556.png)

Nubank is a LATAM neobank, which started off in Brazil, and has now extended to Mexico and Columbia. Here are some key stats, over the last few quarters:

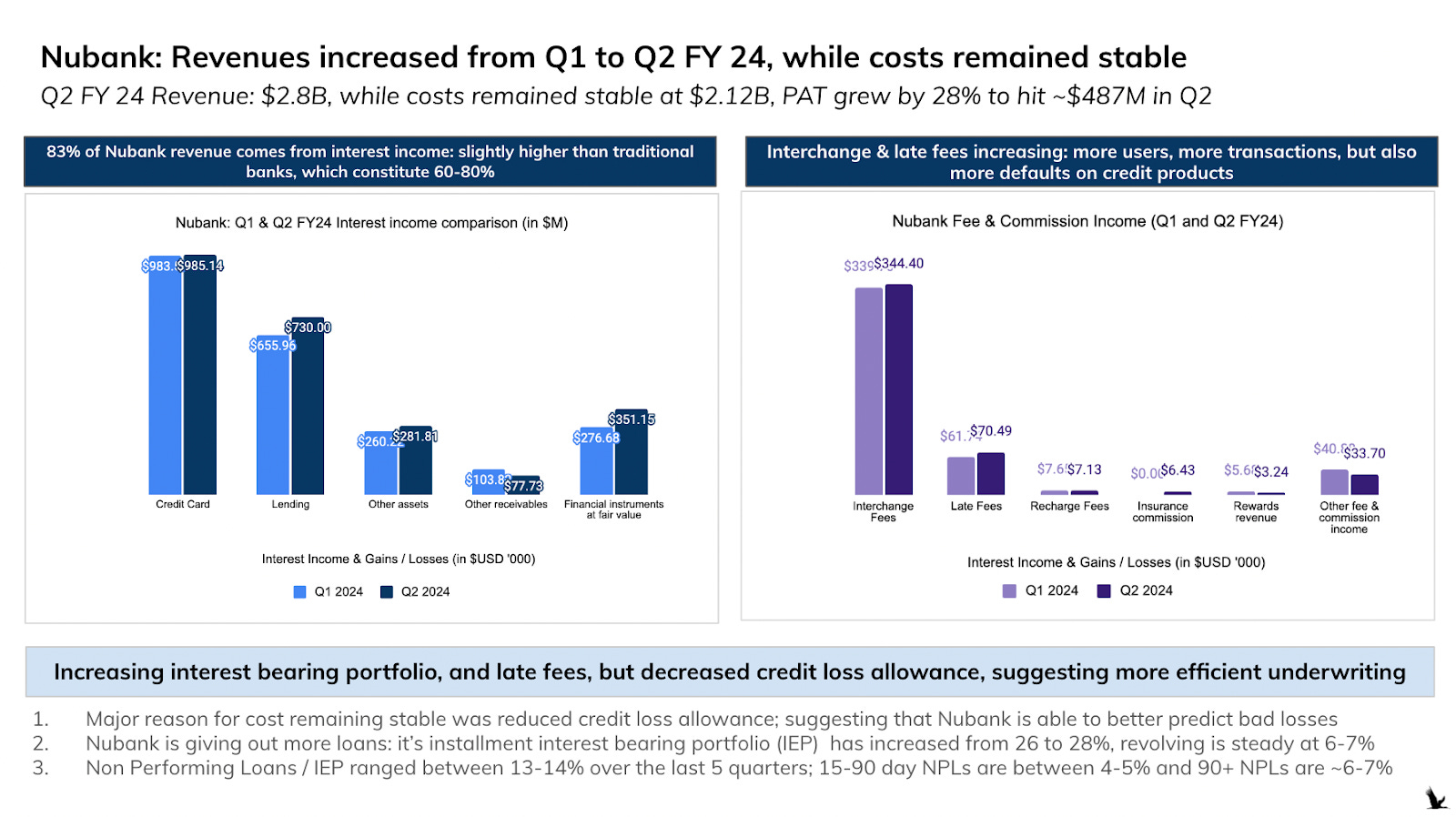

Nubank Revenues:

In Q2 FY 24, Nubank recorded a revenue of $2.8B. 83%, or $2.3B came from interest income and gains on financial instruments. 17% came from fees & commissions, or about $0.5B. Revenue has grown by ~4% growth from Q1 FY24, where total revenue recorded was $2.7B. Interestingly, this seems to be tracking user growth: User growth from Q1FY24 grew by ~5.2% to ~103M users in Q2 FY24.

Note: 60-80% seems to be the component that comes from interest income for traditional banks, so this seems to be in line with the market. Breaking down the key components:

There seem to be some changes in the revenue mix, from Q1 FY24, to Q2 FY24.

Interest income & gains on financial instruments:

Accounts for ~83% of total revenues in Q2 FY24, same as Q1 FY24

Of this interest income, majority components are interest from cards & lending. In Q1 FY24, interest from cards and lending was 60% of the total interest income. This has remained at 60% of total, but the mix has slightly changed: Cards interest income has increased marginally, from $983M to $985M. Lending interest income has increased from $655M to $730M.

This makes sense, if you look at the portfolio, Nubank seems to be pulling back on its cards exposure, in favour of instalment lending.

Late Fees have increased:

From $60M in Q1 FY24, to ~70M in Q1 FY24. They also contribute to a bigger % of the overall revenue mix: From 2.26% of revenue in Q1FY24 to 2.47% of revenue in Q2 FY24.

However, I would be slightly concerned around rising NPLs, and Late Fee Revenue

While its 15-90 day NPLs (non performing loans) seem stable, the 90+ NPLs see are on a rising trend, and hit 7% in Q2 FY24. But its NPL balance as a % of its overall IEP (interest earning portfolio balance seems stable). This NPL of Nubank is higher than what banks in Brazil reported in August 2024, of 3.2%.

Late fees have increased fro $61 - $70M from Q1 to Q2 FY24, and have also increased as a proportion of total revenue

Nubank Costs

The costs in Q1 FY24 were ~$2.12B, which has actually reduced in Q2 FY24. A big reason for this was the decrease in the credit loss allowance which can mean two things: 1) Nubank is lending better or 2) They’re lending the same, but their predictions on bad losses are getting better. Either way, this is a positive sign.

Nubank Profits

But despite the concerns around the Non performing loans, and its profits speak for themselves. They made $378M in profit in Q1 FY24, which grew by 28% to $487M in Q2 FY24.

Neobank risk is higher, but that is to be expected if they’re serving the underbanked.

Let’s also keep in mind, that as a Neobank, Nubank also focuses on providing services to the unbanked. And that can mean higher risk appetite. And what shows promise is the fact that their credit loss allowance is decreasing, implying better prediction models on bad loans, and the fact they’re taking less exposure on credit cards.

Their risk is higher, but thats to be expected, since their TG is risker. They’re willing to take that risk, and depend on their models, and analytics to be able to manage that risk, and actually serve the audience that needs banking infra, not just those who are using it for customer experience. And that’s the whole point of a neobank.

So we can see that Neobanks are definitely adding value in regions where they operate. So what’s happening in India?

The way the Indian fintech landscape is structured, you need banks for everything.

Payments? Better get yourself a sponsor acquiring bank to route payments.

Lending? You need a bank, especially since the risk weights on NBFCs have increased to 125%, and P2P NBFCs are being restricted (although this is for good reason, it was being touted as an investment product).

Banking: you DEFINITELY need a bank. Take the examples of the neobanks in India: Slice, Jupiter & Open were nothing more than fancy packaging that onboarded the customer, and took care of customer service. At the back-end they were partnering with banks to actually open accounts for the customer: and banks operate in a certain way (read: slow to innovate & limited customer first perspectives). Which got frustrating for the fintechs as well. So they tried to get around this by using wallets, and piggybacking on bank PPI licenses, and funding those through credit by NBFCs (either their partner or own). So the wallet would act as a credit account of sorts. Of course, all that got shut down when the RBI circular came out, banning non bank PPI funding through credit lines. But the fact is, that its peak, Slice was issuing 200k cards per month, highlighting a very clear customer need that was not being solved by traditional banks.

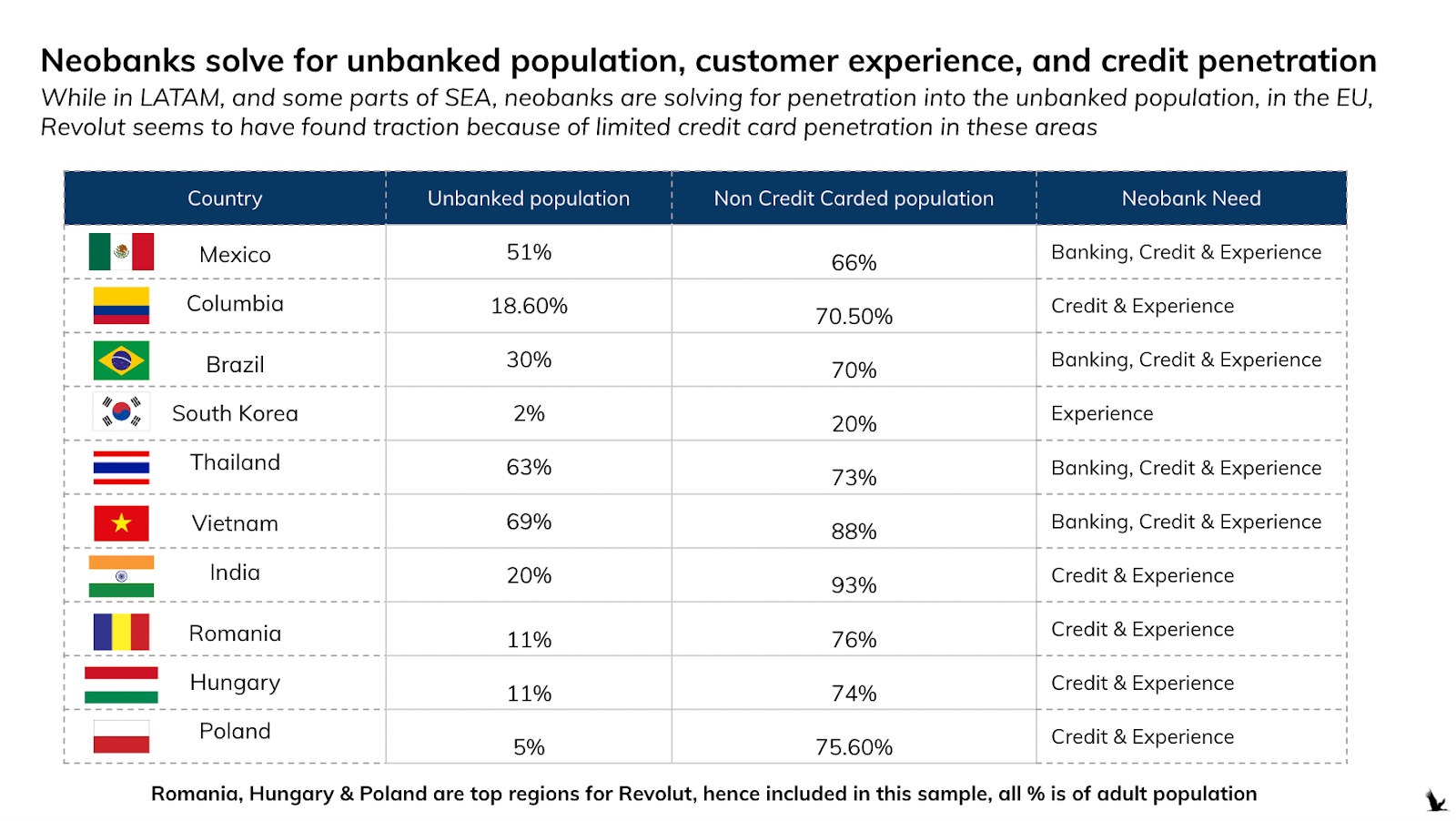

Neobanks solve for credit, banking services, and customer experience

Take a look at the snapshot below: Neobanks across geographies are solving for credit, experience, and banking services. Kakaobank to me is especially interesting, because banking & credit cards in South Korea is fairly well penetrated: 98% of its adult population has a bank account, and 80% of them have a credit card. So what the neobank has come in and solved for is experience: they integrated a popular messaging app called Kakaotalk with their neobanking service.

Fintechs in India are now exploring mergers / investments in banks to solve for the “banking problem”

RBI doesn’t like the concept of a Neobank. They want banks to have physical branches, and some sort of physical presence. So now, fintechs, to streamline their services, either from a payment, a lending or a banking perspective are going after banks for mergers.

Slice merged with North East Small Finance Bank in 2024, 1 year after RBI approval

Jupiter is in talks with SBM India, a subsidiary of the State Bank of Mauritius of 5% - 9.9%

BharatPe and Centrum merged in 2021 to form Unity Small Finance Bank.

And it seems like investors have caught on, and are looking at investing in not just fintechs now, but also banks. Shivalik Small Finance Bank for example, raised 100 Cr in 2024 from marquee investors. And Nainital Bank, a subsidiary of Bank of Baroda is reportedly in advanced discussions with PremJi Invest for investment.

I expect a few more of these to happen in the future. But the key takeway is that unless you have a bank on your side, life gets very hard. And thats why it’s now just Neobanks, but also payment players, UPI Apps such as Paytm who went after a bank license. (Note: Paytm payments bank was banned in 2024 due to non compliance with regulations).

RBI is approving these mergers: so somewhere there must be some agreement that fintechs CAN add value to the banking landscape.

All these mergers of banks & fintechs require RBI approval. So somewhere, there is alignment that a bank, that has a fintech first view, will add value to the ecosystem.

Currently Indian regulations do not support a digital only bank. But I’m sure policies can be worked out. Maybe, even starting out with a Small Finance Bank license, and after meeting subsequent metrics, be upgraded to a commercial bank license. With some minimum requirement of physical presence. This will also enable spreading financial inclusion in specific regions.

My view: Giving neo-banking licenses could actually incentivize banks to get back into the innovation game, and turbo charge the banking landscape in India.

Right now, there seems to be some complacency in the bank world. The view is: let’s wait and see what happens, and then once the landscape is mature, then we can come in and figure out our game plan.

So it’s a wait and watch game. But should that really be the case? Should banks not be incentivized to be at the forefront of innovation, or atleast support fintechs that are trying to do so? Globally, there are examples of neobanks that are thriving: and have not just given a better experience to the customer, but because of their appetite to take risks, and non traditional ways of looking at banking, have actually deepened financial inclusion.

If there is a structure to award neobanking licenses to fintechs (with the requisite regulations), this suddenly threatens the bank core business, and actually motivates them to start thinking about what to do to set themselves apart. Maybe this will even speed up innovation.

Take what happened in Brazil, because of Nubank: Nubank’s popularity has forced banks to step up their game, and invest in new technology.

Brazilian banks were notorious for poor customer services, and very high fees. When Nubank came in, it first started out as a credit card issuer (it partnered with Mastercard for this). Within a year, more than 1 million people had applied for a Nubank card. To protect its losses, Nubank would take very low exposure on customers, sometimes as low as $14, and only raise the limit if the payments were timely. They also used alternate data: not just the credit score, but also payment & transaction history to gauge what this limit should be.

It faced some hurdles in getting a banking license in Brazil because of a law that prevents foreign bank ownership. But in 2017, after a presidential decree gave it an exemption from foreign ownership rules, Nubank received a Brazilian banking license. Now it could offer its checking and savings accounts—all digital.

And this has actually made Brazilian banks up their game: they are now investing in technology, digital experiences, and lowering fees.

After seeing how Nubank actually benefited the financial system, the Central Bank of Brazil, gave Nubank a banking license (and exempted them from certain requirements

Nubank was able to positively benefit the ecosystem, and based on its performance, it was given an exemption on foreign ownership (due to foreign investors), and the lack of physical branches. The Central Bank of Brazil saw the value of a digital banking model, and granted Nubank a banking license, as long as it complied with other regulatory requirements.

So why can’t we have the same in India?

Current bank personas don’t solve the problem.

There are 3 types of banks in India currently: Payments Banks, Small Finance Banks, and Commercial Banks. The “Payments Bank” probably comes closest to what Neobank’s are aiming to solve, but if they actually are solving for this, through tech first innovations, keeping customer experience at the forefront is a massive question mark.

The key problem is, that all of these players are banks first, and then fintechs. There needs to be a fundamental change in the type of thinking. Neobanks globally have succeeded because they were fintechs first, and then banks. They focused on innovation, adopting new technologies to drive adoption (See: Pix & Nubank), and customer experience. And thats what drove adoption and financial inclusion.

Since banks are the cornerstone of everything: This change in mindset is something that drives innovation not just across consumer facing financial inclusion, but also around payments, credit underwriting, and customer experiences.

The need for a 4th License that solves for what is missing now:

Changing the requirements for existing licenses could be challenging. It would require existing entities who have obtained that license to make changes, which, considering they are not really that “tech first” may be hard. So its easier to create a 4th type of license: “The Digital Banking / Neobank License.” But regulators need to have a future first view, and not be bogged down by what has “always happened.” And initially to start off there may be a need to give certain exemptions to promising fintechs in the neobanking space. Like what happened with Nubank.

There can be a minimum requirement: For example:

Have minimal physical presence: If RBI is against online only, then the requirement can be to have 1 physical office, that customers can troop down to in case there are issues, and the rest of the operations are taken care of digitally.

Public reporting of the customer NPS: (Nubank for example trends at 86, which is much higher than other banks at Brazil, which trend at ~40-50).

Handed out on a case to case basis: Fintechs have to demonstrate proof of operations, customer distribution, and top notch customer experience. Only then is this something that they will be considered for. Its not something that randomly fintechs can apply for: Not like the license aggregation game that fintechs are playing (you can check out my piece on this below)

![[#37] Do all roads in fintech lead to license aggregation: Part 2](https://substackcdn.com/image/fetch/$s_!0EZL!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F2cc9aa1e-f79a-469c-9887-52c189f6637f_1634x918.png)