[#46] Will Lightning Strike Twice? Will Jio Disrupt the Streaming Industry Like it Disrupted Telecom?

Unless they solve for original content & platform experience, just acquisitions may not be enough to win

There’s been a lot of consolidation talk in the market over the last couple of years, with many mergers & acquisitions actually happening in the streaming world. Seeing the margins, and especially India being a price sensitive region, this makes sense. Operating in a niche area, and expecting some sort of subscription revenue coming in from users has not worked out: and the user tolerance for the number of activated subscriptions at any given point is not going to be more than 3-4.

Also from a business sustainability perspective, it may not be possible for more than 4-5 players to sustainably operate. Disney + Hotstar lost INR 748 Cr in FY23. (Although Netflix is seeing success, its profit increased from ~35 Cr in FY23, to 54 Cr in FY23, so clearly they’ve figured something out: my bet is on the experience)

Other acquisitions that have happened in the market are:

Amazon Prime & MX Player: Amazon bought MX player to merge with its Amazon miniTV offering: it’s AVOD offering. The deal was reportedly for $100M, and was completed in October 24

Amazon Prime & MGM: In 2021, Amazon announced its acquisition of MGM (Metro-Goldwyn-Mayer) for approximately $8.45 billion. While this is a global deal, it added a lot of content to its India library also

Sony & Zee merger called off in 2024: Sony & Zee have been trying to close this for more than a year, but finally called it off in August 2024. The deal value was reportedly ~$10B.

Voot & Jiocinema: Viacom18 was a JV that happened in 2008 between Network 18 & Viacom. In 2018, Reliance acquired a controlling stake in Network 18. Reliance owned TV18 & Network18 merged effective April 2023. When Reliance acquired a stake in Network18, it became a significant shareholder in Viacom18 as well. Jiocinema was owned and operated by Reliance, and Voot by Viacom18. As of 2023, Voot started winding down, and migrating its content to Jiocinema.

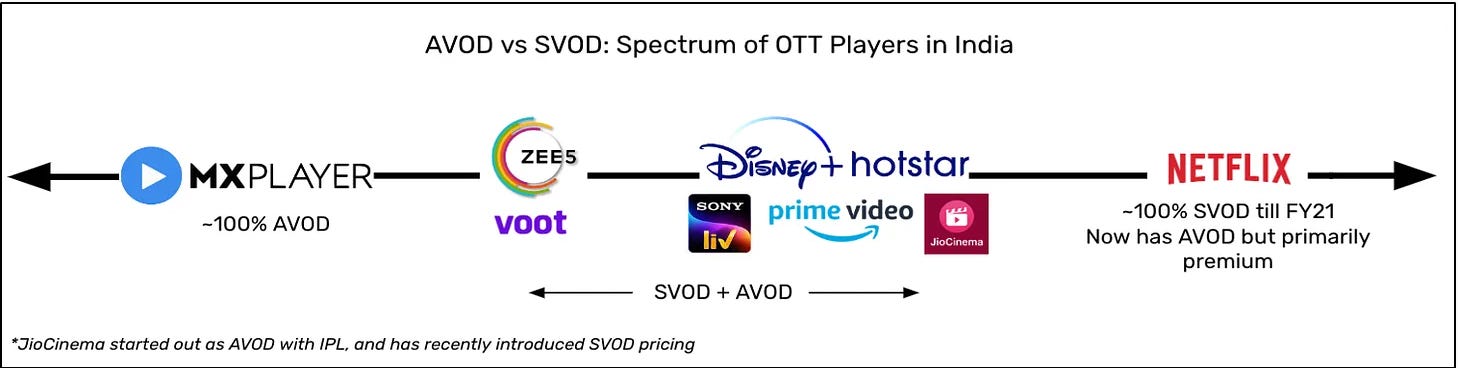

Here’s a view of the different streaming players in India.

You can also check out this piece I wrote on the OTT market landscape in India last year:

![[#2] The User Wars: Where is the next wave of growth coming from?](https://substackcdn.com/image/fetch/$s_!yC6r!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F9498be94-dfcc-4dbb-af80-2d3ca74fd5d3_1509x842.png)

Consolidation as a theme has been going on for a while:

So consolidation has been an ongoing theme in the market for quite a while. And especially with Disney+Hotstar losses, and the fact that it lost IPL for the 2023 - 2027 cycle is when some of these consolidation talks started becoming more than just conversations.

This is the first merger of its kind, where 2 so-called “giants” are merging. MX Player, Voot, and even SONY & Zee weren’t really big in terms of market share. But Jio & Hotstar are. And that’s probably why the Hotstar acquisition by Jio is the talk of the town with market analysts predicting the Jio+Hotstar combination will disrupt the industry as a whole.

A lot is stemming from the fact that Jio has done it in the past - with Telecom

In 2016, we witnessed a unique form of disruption, Jio didn't just enter the telecom game - it flipped the entire board. No new tech, no fancy innovation. Just a pricing move that shook the mobile telecom industry to its core in a race to the bottom. And this made it leapfrog over other players, to capturing 40% market share in the telecom industry in 2024.

How this this happen? Well, in September 2016, Reliance Jio launched with an unprecedented offering: free data and calling services initially only till September 2016 and later extended to March 2017. This transformed the Indian Telecom market, revolutionizing mobile data consumption and paving the way for the way India consumed content. But they were able to do this because they had the funds to undercut: deep pockets to win the pricing war, and capture users.

Game changed:

This strategy triggered a dramatic consolidation in India's telecom sector, reducing the number of major players from 5 in 2016 to 3 (2024) , with Jio emerging as the dominant force (a whooping 40%)

The impact on pricing was equally profound - voice calls became nearly free, dropping from 48 paise per minute in 2016 to just 3 paise in 2024

Data costs plummeted even more dramatically, falling from ₹25 per GB in 2016 to under ₹9 in 2024, making India's data rates among the world's lowest.

But can Jiostar (Jio + Hotstar) do the same?

Eight years after shaking up telecom, Jio is ready to launch Jiostar, its new streaming platform. Reliance and Disney are merging their media assets in a massive $8.5B deal, creating India's biggest entertainment powerhouse.

Boasting the largest slice of India's streaming pie, Hotstar's commanding 26% market share (~35 million paid subscribers) combined with Jio's growing base of 16 million paid subscribers paints a compelling picture. The prophecy of it dominating the market upon acquisition may not seem like a distant dream.

But we have our reservations.

As “Usual Skeptics” :) we believe there is more to evaluate before we jump to the conclusion that Jio+Hotstar will strike again. It has its own weaknesses that can become a barricade to their growth.

Subscriber base will anyway come through live sports & upcoming IPL, so it’s unlikely that they will convert any “new subscribers:” that aren’t already there

There is probably a fair amount of overlap in the subscriber base. Most of Jio’s users probably have a paid hotstar subscription. And secondly, a lot of these users will migrate to Jio, especially in the light of the IPL - live sports are a big driver of paid subscribers. The numbers paint a clear picture: When Hotstar lost IPL cricket and HBO content, 15 million (~12.5M due to IPL and ~ ~3.5M due to HBO) subscribers followed suit. Fast forward to today, and Jio has crossed the same 15 million subscriber mark

So that’s the first question in my mind: If the amount that Jio is willing to spend on live sports will anyway attract users, this acquisition is definitely not for the subscriber base.

And there is paid subscriber saturation leading to more dependance on ads that will impact experience. Ads also may not be enough to sustain the high costs that come with premium content production

The Indian OTT market is experiencing a significant shift in subscriber dynamics, which is a concerning trend for these consolidations. While the overall OTT universe grew by 13.8% to reach 547 million users in 2024, the paid subscriber (SVOD) segment actually contracted by 2%, with total paid subscriptions falling from 101.8 million to 99.6 million.

In contrast, the ad-supported (AVOD) segment has strengthened its dominance, increasing its share from 68% to 72% of the total digital universe. This trend suggests that any new entrants or existing players hoping to capture a larger market share will likely need to focus on ad-supported models rather than paid subscriptions. While this shift toward AVOD can help platforms achieve wider reach and generate advertising revenue, it may pose challenges for profitability and content investment, as advertising revenue alone might not sustain the high costs associated with premium content production, potentially impacting the quality and quantity of original programming in the long run.

We anyway complain about the lack of quality content. This will probably get worse if we start moving to ad only models.

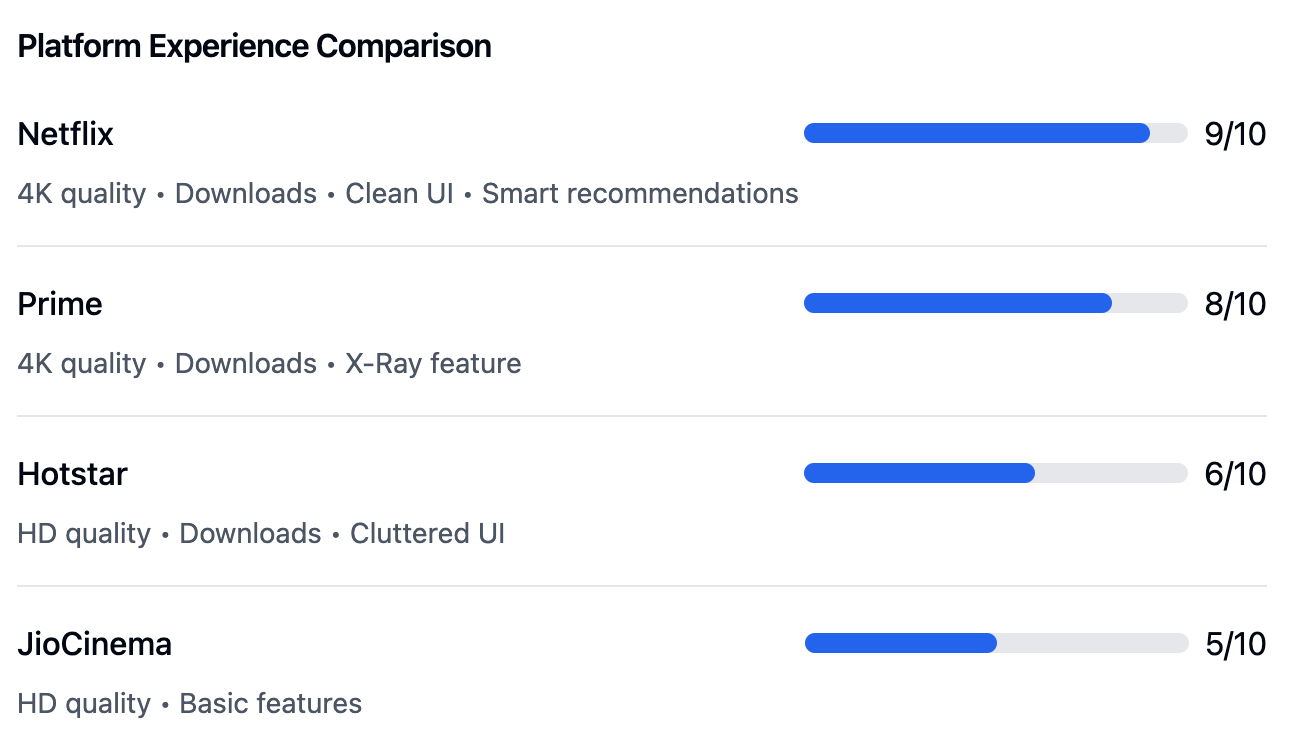

Platform experience is a key driver for subscriber growth - something that Jio lacks as of now, but the fact that they will move to the Hotstar interface is promising

While combining forces sounds promising on paper, the Jio-Hotstar alliance faces significant user experience hurdles. Despite plans to maintain Hotstar as the primary streaming platform, both services currently trail behind their global competitors in crucial areas. In my personal opinion, Netflix probably has the best user experience around - uncluttered interface, and while its recommendations aren’t perfect, they do the job. While Amazon Prime has a different business model - this is one more service that it provides under the large Prime subscription umbrella. But from a user experience perspective, I preferred both Hotstar, and Jio.

This is a personal opinion, but Jio especially struggles with cluttered interfaces that make finding content feel like searching for a needle in a digital haystack. There are also basic streaming issues: watching the Olympics on JioCinema was a nightmare. Navigation & streaming issues, general interface issues, and a lot of cases where it seemed that the server was unable to handle the load, so it would just constantly buffer. To truly compete at the top tier, the merged platform will need to solve these fundamental user experience challenges that have long frustrated their respective audiences.

What’s good is that it looks like Jiocinema will migrate its content to the Disney+Hotstar interface, so at least some of the experience issues will be solved.

But the biggest driver of viewers is content.

And even combined, both Jio and Hotstar lag behind Netflix in original content. So while this could be a content play, I would question: why not invest $8.5B in original content and a better interface?

Netflix successfully navigated the loss of Disney content in 2019 through strong original programming and currently dominates with 33%+ share of top original titles (Omaxe report- Q2 2024). For Hotstar and Jio, the combined original content contribution of top titles is only 24% indicating a significant gap, with limited original programming makes it difficult to replicate Netflix's defensive strategy.

Platform viewership reflects content strength: Netflix leads with 148M+ viewers for top original titles, while Hotstar and Jio's combined reach of ~100M suggests room for improvement

It's not that Netflix has more titles, but based on our personal experience, Netflix does have more engaging content which seems to have higher viewership, and retention: i.e. viewers keep coming back to watch the same shows.

Jio’s strategy is different: instead of focus on original content, they seem to see themselves as an aggregator of platforms: Their partnerships with HBO, Peacock, FX, Warner Bros, and Paramount is what they seem to be focused on.

Content is King (or Queen). Rather than pouring money into new productions, Jio Cinema apparently has completely halted new production deals and frozen content budgets and is prioritizing infrastructure and operational integration over immediate content expansion, perhaps mindful of the traditionally long path to ROI in content production. As someone who indexes very heavily on experience I do agree that this is the first problem that needs to be solved. But I would hope that there is still some investment happening in original content: if not new shows, then existing originals that Hotstar had invested in. While in the short term, aggressive pricing will drive growth, in the long term, the content investment made today is what will drive retention.

There is also a tag of “non-premium” associated with Jiocinema :

While Jio's focus on reality shows like BigBoss, Roadies and Splitsvilla may reinforce a "mass market" perception, global streaming platforms are carving out a premium niche through sophisticated documentary content focusing more on documentaries and docu-series, from heart-wrenching stories of social injustice to explorations of the natural world, to music events, and more.Netflix and Prime Video are heavily investing in high-quality documentaries and docuseries, ranging from social justice narratives to nature explorations. This strategy is evident in successful Indian docu-series like House of Secrets (Netflix), AP Dhillon: First of a Kind (Prime Video), Curry & Cyanide (Netflix), The Hunt for Veerappan (Netflix), and the Oscar-winning The Elephant Whisperers (Netflix). This distinctive content approach helps these platforms maintain their premium positioning and justify their subscription-based model.

Industry insights reveal a clear hierarchy in India's OTT landscape: Netflix and Prime Video emerge as "core subscriptions" that users retain consistently, while platforms like Disney+ Hotstar and JioCinema often compete for the third subscription slot. This behavior points to a fluid subscriber base for these platforms, where users frequently switch their third subscription based on seasonal content like sports events or specific shows. This pattern is particularly evident in Hotstar's post-IPL subscriber fluctuations and Jio's event-driven spikes, suggesting that despite their vast content libraries and regional offerings, they haven't yet achieved the 'must-have' status that drives stable, long-term subscriptions.

So then the acquisition could be for the regional content, but that alone may not be enough to win

While Disney+ Hotstar hosts over 8,000 hours of regional content and JioCinema claims a 15,000+ hour regional library (Industry Reports 2023), engagement metrics tell a different story.

According to FICCI-EY data, only 18% of Hotstar's daily active users consistently engage with regional content outside of sports events, while JioCinema sees just 22% retention for its regional offerings.

And while YouTube captures 95% of regional video consumption, regional content production costs have risen 25-30% annually, and platforms face an 80% churn rate among regional language subscribers.

The data suggests that while regional content is strategically important, it's not yet a reliable driver of sustainable subscriptions.

This is further emphasized by the fact that 65% of regional language viewers prefer free, ad-supported content, making it difficult for premium OTT services to justify their high content investments.(KPMG). Even with south Indian languages contributing to 50% of OTT video consumption, most of this viewership gravitates toward free platforms rather than premium subscriptions.

JioStar still has a lot it needs to figure out - unlike telecom, pricing alone will not be enough

Sure, the aggressive pricing strategies including potential free tiers with ads and ultra-low-cost subscriptions bundled with Jio services may cause a spike in the viewership and active users. And the merger's combined content library of 200,000+ hours will force competitors to either consolidate or exit. Not that there are too many left anyway: but Zee & Sony will have to figure out what they want to do here. But experience is key. At the end of a long day, I want to log onto a streaming platform, and watch my favourite show, not wrestle with ads, experience issues, and a cluttered interface.

And unless JioStar is able to solve for that, it'll never be able to drive the loyalty and the long term retention that Netflix seems to have figured out. Jio's whole strategy seems to be acquisitions. Together, its main offerings are actually 5 international platforms - Warner Bros, FX, Peacock, Paramount and HBO. And then cricket. So when Netflix declares that its coming out with a new original slate, Jio isn't really bothered. It's response is - cool. And other than this, it's looking to bankroll big movies.

But regardless of success or failure: Based on their content strategy, it seems like Jio is where original shows will go to die.

| A guest post by

|