[#53] Neobanks, eSIMs & Telecom: The rise of sticky financial ecosystems

There seems to be a trend; global fintechs (ex: Nubank, Revolut) are venturing into telecom, either by becoming a MVNO, or through eSIM partnerships to increase customer acquisition & retention

There’s been an interesting trend coming up in the last few years in the fintech ecosystem, especially global neobanks. These fintech players which started out with some sort of core fintech offering: neobanks, or some sort of super app, have also started venturing into offering telecom services to the end customer. By that I mean, some sort of mobile network / data connectivity offering. And this is all on the backs on eSIMs. (I’ve talked in detail about what eSIMs are later in the piece).

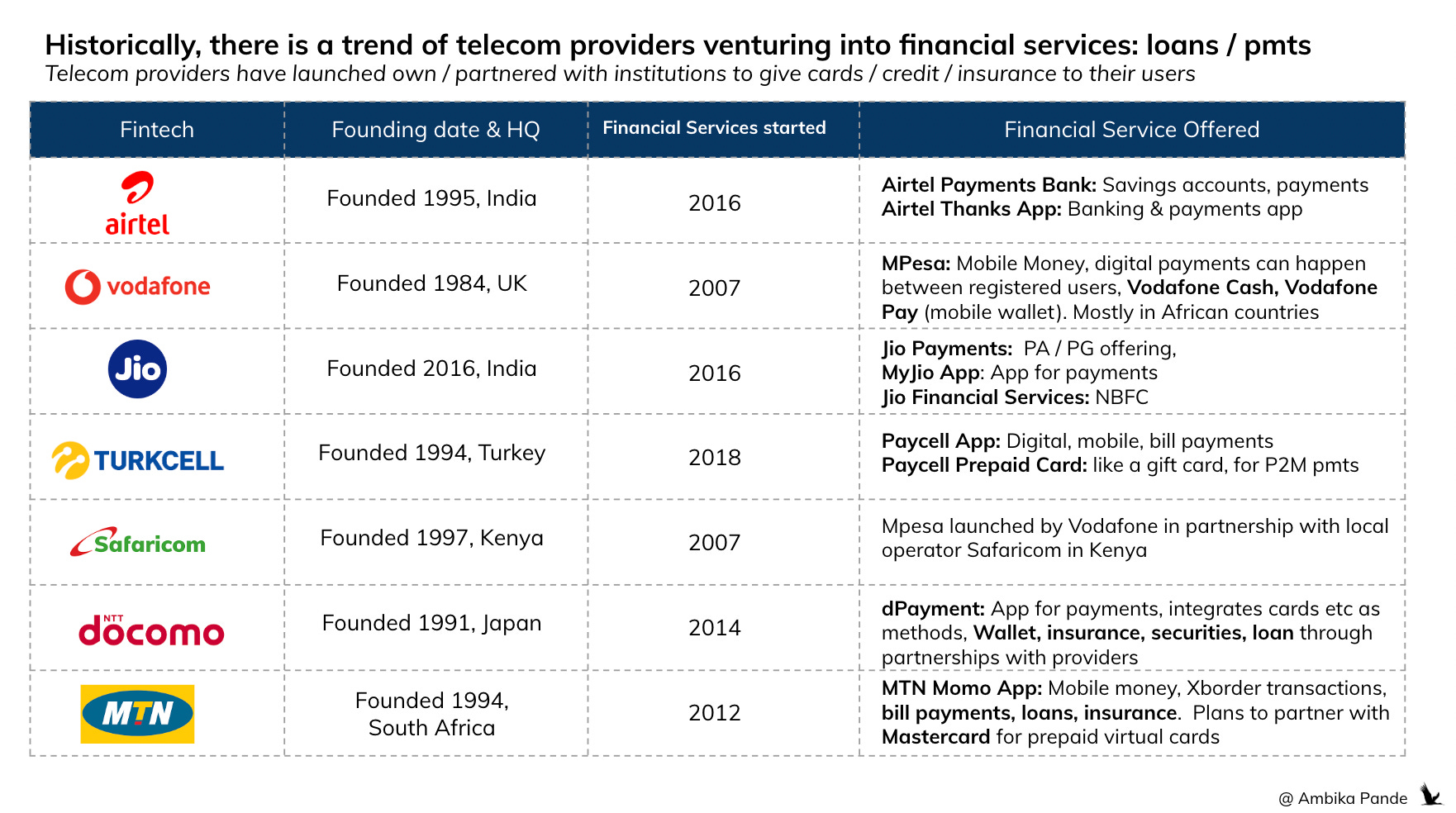

Historically, there seems to be a precedent of telecom players getting into fintech services: loans / payments / banks

Telecom services / mobile data services is something that everyone with a phone uses. And as mobile phones & smartphones have become ubiquitious, (India has 46% penetration, or ~650M smartphone users), this is a service everyone needs, for basic connectivity, and to go about everyday activities. So automatically you have distribution across the mass market. So, cross-selling products seems to be a natural leveraging of this distribution: the primary products being financial ones: things such as cross selling loans, payments, prepaid cards, and even credit cards. Take a look below: telecom operators which have expanded into financial services.

1. Airtel: Was founded in 1995 in India, and launched financial services, such as its payments bank, and its App in 2016 - 2017. The payments bank is like a small scale bank that allows customers to open savings accounts etc. And with it, it launched its App, which operates like any consumer payments app in India: can be used for UPI, checking transaction / bank account history etc. Reportedly 155M people use Airtel Payments Bank (and I’d assume a significant % use the app).

2. Vodafone: Pioneered MPesa, which is a mobile money offering. Users can go to registered retail stores, sign up for Mpesa, and then deposit cash. An equivalent amount is sent to the user’s Mpesa account, which can then be transferred to other MPesa users digitally. This is used in African countries, more than ~60M people in Africa use Mpesa.

3. Other examples: Turkcell in Turkey (founded in 1994) launching Paycell in 2018, which allows payments, and also has a digital prepaid card. NTT Docomo in Japan: has a payment app called dPayment, and apart from payments, method linking, also offers services such as insurance, securities etc. And MTN, launched the MTN Momo App in 2012, which allows for digital payments, cross border transactions, and also plans to partner with Mastercard for prepaid digital cards. Paycell users: 7M (~8% of population), and MTN Momo App has 11M users in South Africa (~20% of population).

So somewhere, telecom players seem to have tapped into their distribution to give financial services to their end customer, at a fairly significant scale.

Global trends now suggest that the opposite has also started happening: Large fintechs are tapping into telecom services to make their product more sticky

Big fintechs, primarily neobanks, such as Nubank in LATAM, Revolut in UK & Europe, and Bunq, in the Nederlands are all offering Telecom services, through partnership with Mobile Virtual Network Operators (MVNOs), or by becoming a MVNO themselves by leveraging “Telecom as a Service” players such as Gig. They leverage these players to provide eSIM services: activation & management of SIMs remotely, both from a domestic, and international travel use case.

(note: i’ve explained all these jargon terms in the next section)

And this is expanding from just a fintech → telecom movement to superapps who want to create a sticky ecosystem for their end customer. Grab, which is a superapp specialising in rides, and food delivery operates as a MVNO (using Gigs). Google launched their own MVNO service in the US called Google Fi (using T-Mobile & other US Cellular infra) in 2015, after they launched their consumer app offering, Google Wallet in 2011. Paytm tried to merge their payments bank with Airtel in 2023, but this fell through. If this had happened, I expect some sort of reseller / partnership type model which bundled fintech & telecom services together would have been figured out.

Quick KT here on some of the “jargon” terms used:

eSIM: At the heart of all this lies the eSIM. So earlier, and even now, many of us, if we want to use another network, or lets say, get onboarded on a local network while travelling need to buy a plan from another network provider, and then physically swap out the SIM, or in the case of a dual SIM phone, add another one. This also has security issues - swapping out the SIM etc. Enter the eSIM. The eSIM is a physical circuit chip soldered on the device motherboard. This is done at the time of manufacture, and not something that can be added later. It allows remote SIM provisioning - users can swap telecom providers without needing a physical SIM, and multiple profiles can be stored on the chip. So theoretically, if I have a device with eSIM functionalities, I just need to be able to go to an app, buy the plan, and activate it remotely, instead of having to swap out SIMs. eSIMs can handle anywhere between 2 - 20 profiles, but at max, from what I understand 2 active profiles can be managed.

There’s a device capability angle as well here: While eSIM as a concept has been around since 2010, this really started taking off in 2016, when Apple adopted it, and started offering it in some of its models. It’s also a way to be more “space efficient”

As per this source, all major manufacturers have multiple devices that are eSIM enabled. Apple, Samsung, Google, Oppo, SONY, Xiaomi, and so on. And most top networks also provide eSIM capabilities. Airtel, Vodafone, Jio etc. There are other players such as Saily (HQed in Lithuania), Airalo (HQed in Singapore), and Nomad (HQed in the US), that provide eSIM services in India. Airalo for example, works with Jio to provide eSIM services, you can basically download the apps of these entities, and activate the required eSIM plan. Airalo though got banned in India in Jan ‘24, due to fraud issues, reportedly, fraudsters were using these e-SIM apps with international numbers to defraud people. So atleast for pure eSIM players that’s something thats important to watch out for, and needs proper sign off from the Department of Telecommunications (DoT).

MVNO: Mobile Virtual Network Operator. Operates as a Mobile Network without its own physical infra, instead, leases this from MNOs (mobile network operators). They operate under their own brand name, and set the prices. They also handle all the pieces related to the customer: billing, marketing sales, customer support etc. Example: NuCel, which uses Claro’s (Brazil telecom network) infra, Google Fi, which uses T-Mobile infra.

Telecom as a Service (TaaS): A key example here is Gigs ($73M funding in Dec ‘24, and valued anywhere between $300M - $400M) gives “telecom as a service” allowing any player to launch / integrate seamlessly with a MVNO. They do all the work of leasing infrastructure, partnerships with multiple telecom providers, and API solutions that allow companies to integrate telecom services into their consumer facing offering seamlessly. This is what Nubank, Bunq, Zolve & Grab have done. They’ve integrated with Gigs to either become a fully fledged MVNO under their own brand or a reseller sort of model, but in both ways, they’ve increased. the convenience of network management through a customer friendly app. : Operating as MVNO’s are: NuCel for NuBank’s Travel eSIM, or Zolve Connect for Zolve’s international telecom offering to immigrants. Reseller model: Bunq has leveraged Gig APIs to offer eSIM functionalities on its app, but more from a reseller perspective, not an MVNO perspective. A point to note: a key investor in Gigs is Ribbit Capital, which is a fintech focused investor. Yet another indication of synergies between fintech & telecom.

There’s a reason why now global fintechs are getting into telecom services. It’s a need of every user, and a sticky product

Using mobile networks is a pain in India. We’ve all had experiences, where we’ve seen challenges in either changing numbers, or SIMs, or activating a different plan. I know I have. And that’s because most telecom players (like banks), aren’t really very customer first. It’s a painful process for the customer just to activate and manage. And I’m not even getting into issues such as data connectivity etc. You’ll go to certain areas, and only Jio will work there. Somewhere else: only Airtel. It’s a headache.

With an eSIM model, coupled with a user friendly flow on a consumer app, you can actually manage all of these issues much better.

Activation & Management of my Data Plans: I still don’t understand how the Vodafone app works. It’s messy & clunky, and not user first at all. There’s a reason why UPI Apps came in, and one big value add that really clicked with customers was utilities payments. Expanding this to eSIM management, so that I can log into an app seamlessly, activate my SIM, and manage multiple profiles remotely is a definite value add.

Solves for mobile connectivity across India & network connectivity orchestration: The reason I don’t have multiple SIMs right now, is that I perceive it as a massive hassle. I don’t even know where to begin. Through eSIM, and convenient management through a fintech app, I would be able to manage multiple SIM profiles. AND, there’s something else that can be done here: if there is a middle man, such as a consumer app OR some sort of TaaS player, you can solve for network switching / data orchestration flows. As a user, I want to automatically connect to whatever network I have better connectivity on → if an app / infra player can manage this seamlessly, and then bill me only for the data and network usage, it makes it more cost effective for the customer. Instead of having to pay for 3 separate SIM profiles, I can pay some minimal fee for activation, and based on orchestration pay only for what I use.

Way more cost effective during travel: While travelling overseas, you either activate international roaming on your domestic network, or you can buy a local SIM once you land, along with a plan. With eSIMs, you can buy a local network plan (in whatever country you plan to travel), and activate it through the app. This seems to be a big hook, and is why NuBank launched NuCel, its MVNO using Claro (Brazilian telecom provider), and its travel eSIM product using Gigs.

In the past I’ve tried to understand what new challenger apps in India & the world use as their differentiator. With 95% of the Indian market with the top 3-4 apps, what can newer players use to differentiate themselves?

I’ve written a couple of pieces in the past on this, you can check them out below:

![[#47] UPI in Nov '24: Challenger apps Super.Money & Navi are challenging, but there is still much to do](https://substackcdn.com/image/fetch/$s_!Qj97!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F93e1deda-9e3c-4cbc-9504-88df29bbd756_1576x884.png)

![[#38] Is the battle for the ubiquitous UPI app over? : What do the next few years look like for UPI Apps?](https://substackcdn.com/image/fetch/$s_!R6jp!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F698a0f5a-e30f-47a6-8be3-e000b9a13819_1600x892.png)

But TLDR, what both these pieces have tried to do is understand, what is the play for the 75+ UPI Apps operating in India? How are they differentiating themselves?

The top 3: PhonePe, GooglePay, & Paytm have the first mover advantage. The rest are either focusing on Credit Cards (like how CRED started), Credit (such as Navi, and now Mobikwik), and more of a sector specific play, such as Groww. Others such as Supermoney, Amazonpay, and Whatsapp are part of a bigger platform. And then you have players such as Slice, Jupiter (faux neobanks, now trying to be banks. Slice completed its merger with North East SFB in Oct ‘24, and Jupiter is trying to acquire a stake in SBM Bank).

But how sustainable is this? Credit isn’t hard to give. Credit Card on UPI, is just another method connected on UPI rails, so I don’t understand what players such as Kiwi are actually using as their differentiator. Rewards is a “burn & earn” sort of play to acquire customers. All of these things are nice to have for the customer. Are they must haves? Will they make me loyal to a particular app? I’m not sure.

As a customer, I’d say I’m pretty saturated in terms of the number of payments apps I use. So what will make me consider yet ANOTHER app?

And this is maybe where the fintech & telecom play together starts making sense, and acts as a differentiator to set apart Challenger Apps

Will I use another app just for payments / credit / rewards? Maybe not. And even if I do, the minute this model sees PMF is when your PhonePe & GooglePay’s of the world will implement it. But if you give me a way to manage my mobile data plans / activate networks / manage networks & network orchestration in a seamless manner, suddenly things get a lot more interesting.

Real time cross border payments are still nascent. I’d say, while we have a winner in the Indian domestic UPI App space, the market for cross border & international real time payments in India atleast is still open. And when you add managing mobile networks while travelling internationally, this could be a differentiator.

At least, that’s what some top consumer apps and Neobanks of the world seem to think.

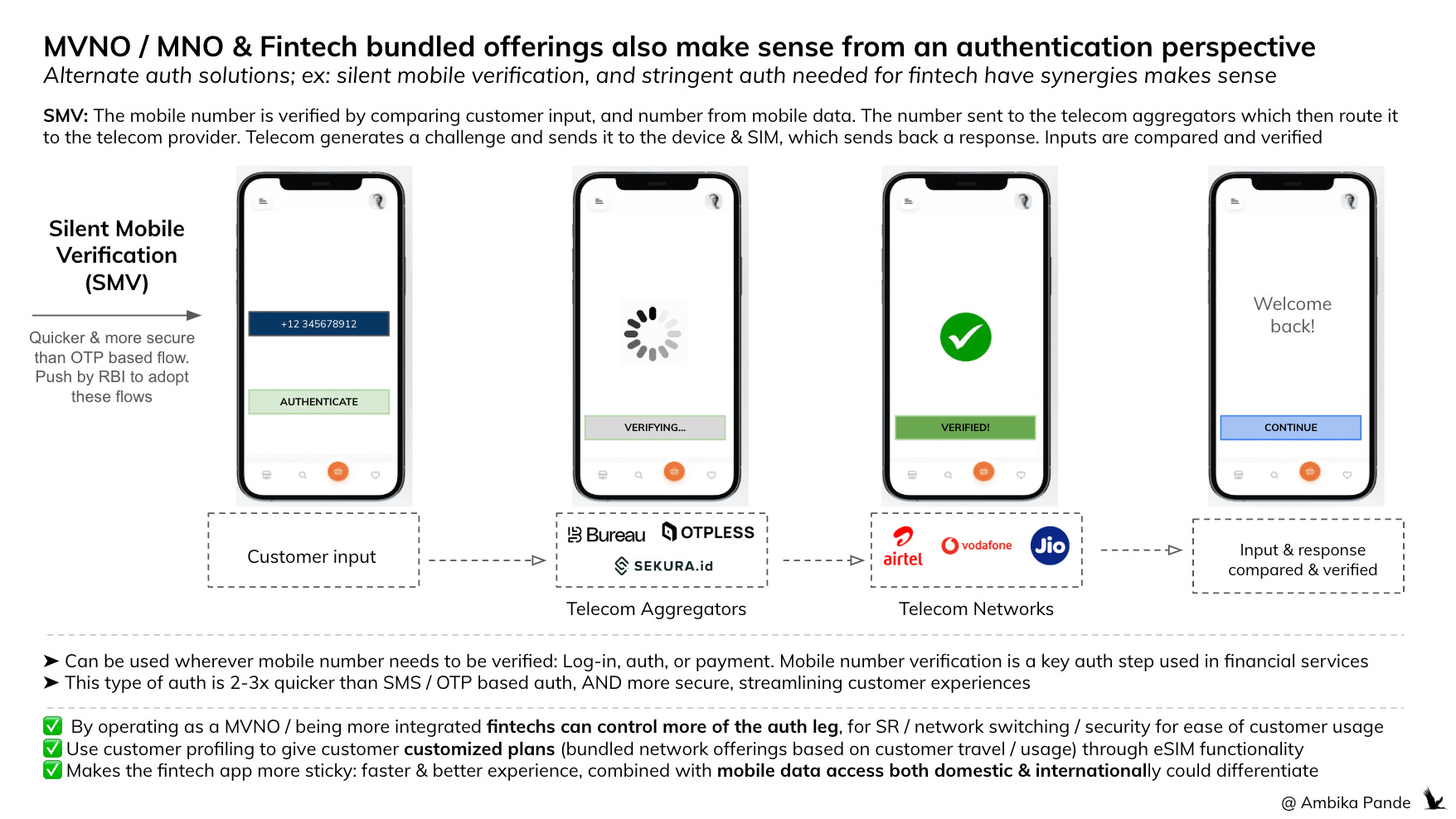

There’s another interesting angle here: that of authentication. Secure verification of the mobile number is key in financial services & payments, which can be facilitated through mobile networks

Mobile number verification is a key part of any flow. It’s a key identifier: be it Aadhar / PAN verification, from a log-in perspective, and even in payment flows: Example, when you pay through card, you get an OTP to your mobile number. When you set up a UPI App, you go through something called device binding, where you register your mobile number and device with NPCI, so that you can make payments only using that device & SIM. But OTP is susceptible to phishing, takes time: 5 - 15 seconds to actually get the OTP on your device, and there is increasingly a push to move to alternate forms of mobile number authentication by RBI.

There’s a new form of authentication called Silent Mobile Verification: where instead of verifying the mobile number using SMS / OTP, you can verify it using mobile networks. It’s faster, and more secure than OTP based authentication, bringing authentication times to < 2-3 seconds. You can check out the image below to get a since of how it works.

The way Silent Mobile Verification (or SMV) works is that a customer enters their phone number, which is sent through telecom aggregators to telecom networks.

Telecom aggregators here connect to all the different networks: in India, this is Airtel, Vodafone & Jio. Prominent telecom aggregators are Bureau.ID (Raised $30B in 2024 in Series B funding), Sekura ID (a prominent global player), and OTPLess. Note: BureauID raised its series B funding, in part from Quona Capital, which is a fintech focused investor. And as I mentioned previously, Ribbit invested in Gigs, a TaaS player. So increasing, the market & investor sentiment seems to be that fintech & telecom in some way are becoming a converging offering.

The telecom aggregator routes the masked / tokenized customer mobile number to the network. The network then generates a challenge that is sent back to the customer device & SIM, which sends back the response using mobile data. The inputs are compared, and the number is verified. Of course, there are multiple things required for authentication to happen here:

Mobile data needs to be working: If the network is not working then this form of authentication will not work

Mobile network APIs need to be working: If the telecom network APIs are down, or are unable to verify for whatever reason, then this will fail.

Now, if as a fintech, if I am able to own more in this flow, then I can increase success rates of authentication & verification, and overall make the experience for the end customer faster, more secure & seamless.

As a fintech, or a superapp, I have an understanding of my customer. Where they purchase, what they use their app for. Based on this, just from a reseller perspective, I can recommend specific telecom plans, that will enable better connectivity, and thus, faster authentication and payments. Example: I need wifi or mobile data for UPI payments. Based on some sort of eSIM service & adding some analytics / orchestration, I can provide dynamic network switching to ensure that authentication and payment success rates are higher.

And if, as a fintech I operate also as a MVNO or a MNO, then I can optimize my services for my customer. Since I have some control on the mobile network, I can guarantee certain improvements in the experience to the customer, on both auth & payments, because I have visibility on the customer behaviour, and the MVNO / MNO downtimes, and solve those myself, instead of waiting on the telecom network to fix it. And this creates a sort of ecosystem: if I can guarantee these improvements, then it makes the customer more likely to use the fintech MNO / MVNO as a telecom provider. That seems to be the way NuBank is going with NuCel.

Note: SMV currently does not work in a dual SIM method, that is, if the customer number entered, doesn’t match the SIM that is running the mobile data. Usually in a dual SIM scenario, the primary SIM is the number, and the secondary SIM is used just for data. In the case of eSIM, its possible the different profiles have different numbers, so at the start, the dynamic network switching concept may not work from an authentication perspective but as this space evolves, there could be possible solves for this.

In India, the telecom industry is not an easy one to disrupt, multiple issues exist. So for fintech players it may be easier to go the eSIM reseller route, and focus on MVNO / TaaS integrations internationally

In India, Telecom is a duopoly. Primarily controlled by Jio (45% ) and Airtel (25%). Other players are BSNL and Vodafone. High costs of spectrum, limited spectrum available for private players, infra density in urban areas versus rural, and high capex cost & profitability issues may make it tough to operate from a MNO / MVNO perspective. And limits innovation and coverage.

Even to operate as a MVNO, one would need to integrate with these telecom players individually, or use a middle layer such as what Gigs has done internationally. That, from what I understand does not exist currently.

Another challenge in India is that reportedly sonly 10-15% of devices (and these are the high end models) have eSIM compatibility. Compare that to the US which has ~70%. A reason for this is possibly because popular Chinese models in India such as Xiaomi, and OnePlus continue to offer dual physical SIM slots on their devices, primarily because of the stringent rules in China. However growth is expected: by end of 2025, 60% of global smartphone sales are expected to have eSIM functionality - India will be slower, but as awareness grows, this will increase.

But that doesn’t mean opportunities are not there. eSIM services are provided by Airtel, Jio & Vodafone. Reseller / partnership functionalities can be provided through fintech apps for easy activation and management of mobile networks in India. You’d still need some sort of API integration, but this is definitely easier to offer as compared to becoming a MVNO.

From an international perspective, MVNO, TaaS opportunities exist. Such as what Zolve has done with Zolve connect. It’s paired its cross border neobank with mobile network services. It’s leveraged Gigs (TaaS) to provide mobile network services to travellers in the US, leveraging AT&T and T-Mobile’s carrier networks.

Globally, I expect this trend of pairing consumer apps (superapps, fintechs, neobanks) with telecom services to increase, as these players look to make their ecosystems sticker. In India, this still may take a while because of how our telecom industry operates. But providing eSIM activation & management could be a good start.

And it makes sense for fintech players to enter to the telecom side

Edit: 30th April 2025

1. India’s identity stack is SIM first + OTP-heavy, so banks & fintechs are dependant on telecom companies

Everything from UPI to Aadhaar to banking runs on mobile numbers + OTPs. By controlling SIM you can control the authentication layer, and then figure out how to verify the customer’s identity - through SMS / OTP, or new authentication layers such as silent mobile verification. And another key point here, is that because of the type of service that banks & fintechs give, identity is key. So they’re dependant on telcos, s but are locked out of the SIM UX and identity control.

2. Poor telco UX is a financial service risk

I recently got an SMS from my telecom network (Vodafone) that my device has eSIM functionality and that I can follow a simple online process to activate my eSIM. Naturally, after understanding the benefits of eSIM I was intrigued, and figured I’d try it out. But the experience was very poor. I’ve attached screenshots of what the experience was like, and other bigger issues, even if you get over the experience problems.

Stepwise, this is the process:

I got an SMS, but instead of telling me how long the process is & the value prop (something like “Activate your eSIM in < 1 min and get access to XXX), I was told to trigger the process by sending an SMS to 199, and a random link for more information. On clicking the link I was redirected to a page which gave me some information on what eSIMs are, but for a “not well educated or interested” user, you’ve already lost me at this point

I send the SMS: eSIM <space> ambika@xxmail.com to 199, and get a response back to 1) consent via SMS 2) consent on autogenerated call and 3) scan the QR code on my registered email. Already I see multiple issues here:

I was not told what the SMS content needed to have to consent via SMS. So I was dropping off, and then as a last resort checked my messages again. There I saw ANOTHER sms has been sent telling me the content of the SMS I needed to send to give consent for eSIM activation

I then had to consent on autogenerated call by clicking “1” on the keypad. Not a huge issue, but why is this required? I’ve already consent via SMS

I then have to scan the QR on my registered email ID. I see a massive problem here. Most people have multiple email IDs. And we’ve had the same number for a while, chances are that I don’t remember what my registered email ID is for my number.

So immediately, multiple issues from a product & adoption standpoint. I’m not well educated on what this is, the step steps to activate this are not clear, and ideally should JUST be routed through my number.

And that’s not the only part → there are post activation issues which prevented me from actually activating my eSIM

Activating an eSIM typically takes several hours to 24 hours.

During this time, your SIM may:

Lose SMS and call capability temporarily (especially outbound).

Block you from receiving OTPs, which in India are critical for banking, UPI, payments and 2FA.

Have unreliable or no mobile data for some duration.

Most telecoms (Airtel, Jio, Vi) do not clearly communicate this downtime, which causes confusion and lockouts.

This delay is partly due to TRAI-mandated cooling-off periods to prevent SIM swap fraud, but the implementation is user-hostile.

And because India is a 2FA mandated, mobile first country, I’m suddenly restricted for 24 hours (or even more) if there is a blocker

If a user switches SIM or changes eSIM and doesn’t get OTPs for 24 hours, they can’t access their bank, then can’t buy anything, or do anything that requires an OTP

If I have no mobile data, all internet access on my phone is blocked. And for folks who are commuting, travelling, doing internet banking, or anything else on their phone, you’re completely locked out.

So eSIM onboarding in India breaks critical identity/auth flows for up to a day. That's unacceptable in a 2FA-heavy, mobile-first country. And telecoms are compliance-first, not user-first — fintechs suffer the fallout (e.g., locked accounts, failed logins).

eSIM decouples the telco from the SIM, which removes customer lock-in and is NOT beneficial for the telco, and why it’s such a painful experience to activate this

While an eSIM allows the end user to manage multiple profiles from different telco providers, its beneficial for the end user, but takes away the customer lock in from the telco provider. And that’s where the challenge lies. So to actually drive adoption, we need regulators like TRAI to step in and mandate portability and ease of switching. And for new players (fintechs, travel apps, logistics platforms) to step in and embed telecom into their own stacks, using TaaS, and serve as challengers.

And that’s why going forward, I wouldn’t be surprised if I see some challenger superapps / fintechs which are merging with banks / those specializing in lending such as Jupiter (acquiring stake in SBM India bank), Slice (merged with North East Small Finance Bank), BharatPe (merged with Centrum to form Unity Small Finance Bank) and even players like Navi, Cred which are going the superapp way.

Its a real hassle to activate the e-sim! We had it mandatory in my last organisation and I kid you not, I considered resigning just so that I wouldnt have to go through that ordeal! Thanks for this article, its really great!