[#57] The implications of SEBI’s proposal: UPI’s Role in Wealth-tech

Proposed changes by SEBI for UPI, and the profits of investment fintechs could signify 1) the rise of niche UPI investment apps & 2) existing UPI apps pivoting to investment as a core value prop

In the previous edition of the newsletter, I had talked about how UPI incentives for low-value P2M UPI transactions have been cut by ~80%, which is not enough to cover the costs of UPI to the ecosystem. You can check it out below:

[#56] FY25 Budget Implications on UPI (Part 1): MDR on regular UPI transactions is now essential

![[#56] FY25 Budget Implications on UPI (Part 1): MDR on regular UPI transactions is now essential](https://substackcdn.com/image/fetch/$s_!5OAU!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fbdadd201-6844-4b81-b0f1-aadc51680154_1600x903.png)

The FY25 - 26 Budget for India was presented on 1st February 2025. And it came with some interesting developments for UPI. A couple of things drew my attention, and it's something that could impact the ecosystem. They were:

The second news that caught my attention, and will have implications on the UPI landscape has to do with SEBI. They are:

1. SEBI has proposed to increase the daily transaction limit on capital market transactions from INR 2L to INR 5L

2. SEBI has suggested creating a unique UPI address for registered market intermediaries, making it easier for investors to confirm that they are paying only registered entities

3. There’s also a 3rd: SEBI has suggested UPI-like device binding for all the Broking Apps, but since it doesn’t really have UPI implications, I’ve not deep dived on this at this point. But, it’s interesting. To explain this -> Device binding in UPI is a step where you link your SIM and device to your account, so only that specific device and SIM can be used to make a payment. That’s the reason why you can’t use someone else’s phone to access your UPI accounts because of the device-binding step. This happens when you download a new UPI App, and you have to send a SMS, this is your mobile number being verified, post which your device is registered with NPCI). SEBI plans to replicate this for all the investment apps, where no one can access your investment account without sim being present and bonded to your mobile device. This may mean you cannot access and help your elderly by managing their Demat account from a faraway place. And yes, and also all those people who open demat accounts for their entire family, relatives, neighbours etc and use all the demat accounts for applying to IPOs…this is bad news

So what prompted the increase in the UPI limit for capital market transactions?

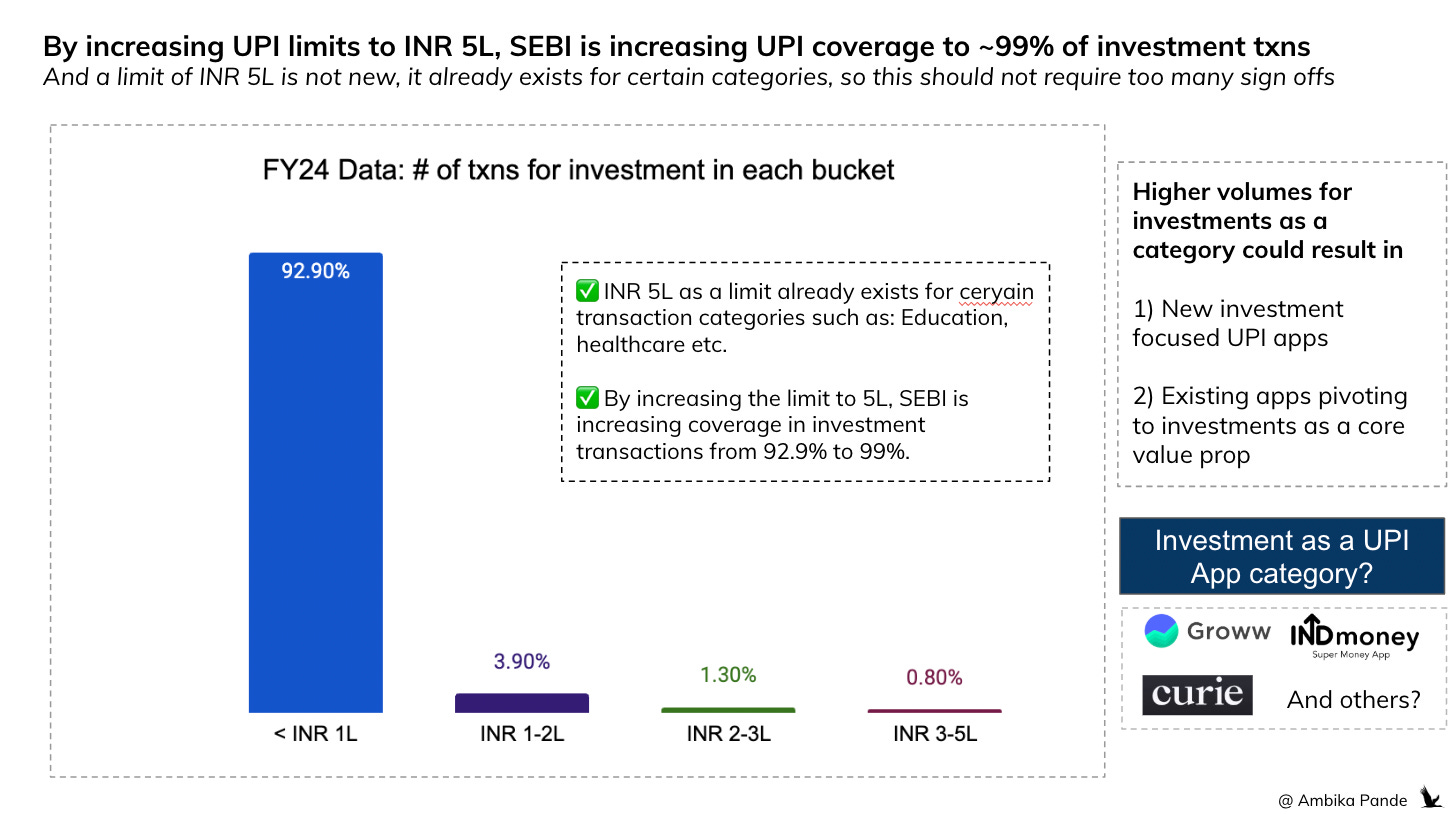

Well, when it comes to the daily transaction limit, the limit of INR 5L already exists for certain categories. SEBI conducted a recent study and has released a consultation paper, which will soon be a circular after incorporating feedback from industry experts. (link to source here)

And the results from this study are what guided this proposal:

1. < INR 1L: 92.9% of capital market transactions had a value of < INR 1L

2. Between INR 1-2L: 3.9% in between 1-2 lakhs

3. Between INR 2-3L: 1.3%

4. Between INR 3-5L: 0.8%

Now, the INR 5L limit already existed for certain categories, such as education, tax payments, IPO schemes and so on, but was not allowed for capital market transactions. So the logic here is that for a small increase in transaction limits, from INR 2L - INR 5L (and 5L as a limit already exists for other categories), SEBI can increase its coverage from 92.9% (which is the 1L bucket) to 99%.

This will further add to the redundancy of Net Banking as a payment method. Today these high-value transactions above INR 2L happen either via Net Banking, Account Transfers, Cheques or NACH. (Cards are not a preferred payment option in investment transactions as Third Party Validation(TPV) is not widely available for cards). However, Net Banking is the most preferred option. When compared to UPI, the ease of usage is much higher for UPI. UPI transactions typically take anywhere between 3-6 clicks compared to Net Banking which can involve as much as 30-40 clicks when you include the login and password complexities. And some providers make it even more difficult with random login IDs which you don’t remember or enter multiple OTPs or enter grid details of your debit card. Allowing UPI for high-ticket transactions will make the payment journey smoother for end investors

But lets take a step back. Why even get into UPI, as an investment / wealthtech offering?

For a UPI App, getting into investments make make sense. Broking apps seem to be the only profitable fintechs (more on that below). But why should investment platforms get into UPI?

UPI is a strong customer acquisition / growth channel

Transaction history on UPI can be a very strong layer of data used to offer personalized products, especially from a fintech perspective

With UPI becoming such a big part of the payments experience, and new innovations coming in, more ownership means more control, and faster GTM, which is a direct input into getting a higher market share.

You can check out the list of licensed PAs, and UPI Apps as of 25th January ‘25 in my piece below.

[#54] Do all roads in fintech lead to license aggregation: Part 3

![[#54] Do all roads in fintech lead to license aggregation: Part 3](https://substackcdn.com/image/fetch/$s_!5-Qp!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F16919966-fc0f-48ba-9510-c26f74ed2638_1744x978.png)

Note: License status updated as of 27th January 2025

So then what does the SEBI proposal mean for UPI & Investments? Well, it could mean several things:

1) More Investment Platforms will get into UPI for ease of transactions, and since UPI payments can only be executed via Apps, they will become UPI Apps / or use UPI Plug-ins

While UPI transactions can be triggered through browsers, or any platform, through an intent or collect request (intent is when you select the app you want to pay through, and are redirected to it, while collect is when you enter your VPA into the website, and a request is generated on that specific UPI App, and you have to open the app and enter the UPI PIN to make the payment)

But the actual payment happens through the UPI App. That’s why investments, as a category for UPI apps, is coming up. You can read more about it in my article below:

![[#38] Is the battle for the ubiquitous UPI app over? : What do the next few years look like for UPI Apps?](https://substackcdn.com/image/fetch/$s_!R6jp!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F698a0f5a-e30f-47a6-8be3-e000b9a13819_1600x892.png)

Increasing the limit of capital market transactions through UPI to INR 5L, which while isn’t a big % of the value processed, could be the push that investment platforms need to become UPI Apps, just to make the transaction more seamless. There are already investment apps that are making/have made UPI moves here:

1. Groww is obviously the leader of the pack here. In January ‘25, It did INR 11.2k Cr of value & 15.4M transactions a month. It launched its UPI App in July 2023.

2. INDMoney is another investments/broking app that recently launched its UPI payments app in December ‘24, doing ~INR 300 Cr in Jan ‘25.

3. Zerodha does not have a UPI App and doesn’t seem to have plans to become one, but it does have a UPI Plug-in (on Juspay stack) through which it powers a lot of volumes.

And I expect newer investment apps such as Stable Money (which is more into FD) to get in here, either from a UPI App, or a UPI Plug-in perspective, to drive better experience.

Curie Money is another new investment app with a UPI play that is coming up (in CUG right now), and trying to do exactly this. Based on its website, it seems to be trying to combine the best of mutual funds, savings accounts and UPI. Their value prop is investing customer money into a “high yield” savings account connected on UPI rails. It seems to have built out a unique flow, where the customers' money is invested in mutual funds, AND this account can also be linked on UPI rails, and used for P2M / P2P transactions. I’m not sure how they are solving for liquidity, since money invested in mutual funds is not instantly available, but it’s possible they’re co-building some of these flows with partner banks, or using some sort of float / instant settlement flow, which is like a super short-term lending product. To understand more about instant settlement, you can check out the Razorpay Instant Settlement product here

The downside here is that if you are a licensed UPI App, you cannot pick and choose functionality (such as only mandates or only autopay), but must enable all the functionalities that NPCI dictates. For category-specific UPI Apps focusing on investment, a lot of these functionalities may not really be relevant and are just additional overhead and costs. A lot of these Apps don’t build their own stack but are powered by Juspay’s TPAP stack (Razorpay TPAP is another option), but there is a cost of integration and maintenance. And hence, atleast to start-off, a plug-in may be a better experience.

Maybe one way to go ahead here is that as categories mature and use-cases get defined, NPCI can dictate specific functionality for specific use-cases to avoid investment apps building out redundant features for their use-case: almost like sub-categories of a general UPI App. But that will take some time to think through. And other categories, use cases & edge cases will have to be defined.

2) Investment Apps may get into a full stack play, and this is where the SEBI proposal of assigning new unique UPI handles to registered intermediaries change has an implication:

What is this exactly? Well, over the last few years, SEBI has been cracking down on the potential fraud and increase settlement speed, in the interest of end investors. Examples of some initiatives in the past:

1) Non-Pooling of Funds: Disallowed brokers to hold investor money in a common pool account, before transferring to mutual fund houses. The goal was to prevent the misuse of these funds. The PAs, banks and all the ecosystem players had to implement new flows for money movement and reconciliation.

2) Direct settlement mechanism: To ensure that funds are directly transferred to exchanges without passing through a middle account of the broker.

Even though there was some resistance from the players in the ecosystem, the regulator pushed through these implementations with the belief that this was good for end investors

And on the same lines, there are some more changes that may happen soon. In the consultation paper released in January ‘25, SEBI has proposed issuing unique VPA handles to all the registered intermediaries like Stock Brokers, AMCs, Mutual Fund Distributors, Research Analysts(RAs), Investment Advisors(IAs) etc. This will basically add an extra layer of verification and signal to the end consumer that they are transferring money to a verified intermediary. SEBI has been working closely with NPCI to get this implemented.

Implementation requires coordination among multiple 3rd parties: a full stack play gives more control and faster go-live times

After implementation, all the registered brokers and other intermediaries will receive their own handle. Example format: zerodha@payrighthdfc. Currently, the VPA is along the lines: zerodha@hdfcbank. And there would also be a verified icon. This will signal to the investor that the payment is being made to the registered entity and that the investor’s interests are safeguarded by the regulator

As an initiative, it’s great. Definitely adds a layer of security and goes a long way in making sure that only verified intermediaries are involved here. But there is a problem. When you’re changing VPA’s as a merchant, you have to coordinate with multiple 3rd parties. The VPA is linked to a current account, so

The merchant would need to update their VPA

Whatever 3rd party they are integrated with (such as a PA, or multiple PAs) would need to update the mapping of the new VPA to the current account and

When a merchant is onboarded onto a PA, they are assigned a VPA, based on the bank from which the UPI terminal is procured. If this is an investment merchant, the logic for new VPA creation would need to be changed.

So this will require coordination and effort from multiple parties within the payment ecosystem. And there is no monetary incentive to do this. And if there are multiple 3rd parties who need to be coordinated with, then it takes time to go live and implement these changes that much more painful. And hence, since UPI is a key payment method, and it’s still evolving, it makes sense to have more ownership across multiple payment & 3rd party legs (such as the UPI App and the PA), to make it faster to go live and be compliant. This is why almost every PA is investing in their own infra play, and their UPI & Card switches. Less dependency on a 3rd party, leads to faster innovation. Same logic applies here

And thats why they may go after a PA license and even an NBFC for Loans Against Securities

Look at Groww, which is doing ~INR 10k - 11k Cr of value a month on UPI. It is a UPI App, has a PA License, and has a NBFC. At those volumes, it may make sense to some to have your own PA processing these volumes. At some scale, the cost of regulation and maintaining can be offset by building your own PA.

There is also another use case that existing brokers have already gotten into, and that is Loans Against Securities. Volt Money is one example: it raised $1.5M in 2023 in pre-seed funding from Titan Capital. As the market seems tough for now for unsecured loans, secured loans are where there seems to be more comfort. Groww is a player here: it has an NBFC called Groww Creditserv with a loan book of $115M as of June 2024 and offers a variety of loans, including Loans Against Securities, both on its own books and through lending partners such as IDFC Bank, Fibe and so on. Zerodha is another example: It has a NBFC called Zerodha Capital, that gives Loans Against Securities as well. So at least for upcoming investment apps, a full stack play: UPI for experience, PA for costs & experience, and NBFC for Loans and other products seems to be a play that is coming up.

3) Investments / Broking Apps seem to be the only big fintechs making money, this could result in more UPI apps focusing on investments as a core offering:

Groww in FY24 was at ~$35M profit. Zerodha reportedly is at $1B. Angel One in FY25 will have annualized profits of $133M. Upstox has $22M profit in FY24. 5Paisa, although a subsidiary of IIFL, had profits of ~$8.1M in FY24. Smaller apps are still scaling: Indmoney for example had losses of $9.7M in FY24. But overall, investment broking apps seem to be the only ones making money.

But it's still better than other fintech segments: PhonePe (one of the biggest fintechs in India today, in the payments and consumer app space) for example, is at losses of ~$240M in FY24, although to be fair, that's because of its ESOPs cost. Without ESOPs, it's ~$20M in profit. PineLabs, another PA, specializing in offline payments, was at a ~$22M loss in FY24 (187 Cr loss).

And this is probably why PhonePe and Paytm have launched their own plays in stockbroking & investments. PhonePe launched Share.market in 2023, which is its in-house stock broking app. Paytm launched Paytm Money way back in the day in 2018.

Another positive: Margins for broking/investment seem to be higher than other fintechs (apart from lending, which comes with its own risk). Revenue streams for investment apps are:

Some % commission from the Asset Management Company (AMC) for buying Mutual Funds (the end customer doesn’t pay here)

Some margin charged to the end customer on stock trading: this is either a fixed fee which is INR 20), or a brokerage of 0.03% of the trade amount, whatever is lower. (this could differ depending on the instrument, and investment type, could be equity delivery, intraday, future & options and so on). Just looking at Groww UPI volumes, assuming majority of its investment volumes comes through UPI (which is fair, it has an AoV of ~INR 5k - 6k which is in line with a monthly SIP, and approximately ~13M users, so this checks out), at a monthly volume of INR 112k Cr in Jan 2025, and ~15.4M txns even if we assume some % of this to be priced instruments, at either INR 20 or 0.03% is still significant

Some annual maintenance charges & account opening charges (could be INR 300 - 800 annually).

Compare this to UPI: While big apps may earn INR 5p - 25p on P2P, and some through incentives on P2M values (which are also decreasing by the way), there aren’t a lot of other ways to make money. And for PAs, the market is crowded: There are 20+ PAs in India, and at an aggregate level, each is probably not making more than 5bps on payment volumes, due to competition.

Broking firms also used to earn through float income, which is another lucrative stream of revenue, although regulators are now cracking down on these avenues:

Broking firms also used to earn a lot of money through float income. Take for example a Groww or a Zerodha. Because these apps aren’t banks, the way you invest in stocks through their platform is by loading the money into a wallet, and then using the money in the wallet to invest in securities. If you use broking platforms by banks it’s different: for example HDFC securities, I can directly link my savings account to my trading account and transfer money. And maybe that’s one of the reasons why Zerodha has applied for a banking license (but got rejected). Now in the case of non-bank brokers, there is some money that could possibly be left in the wallet that is not utilized. Broking firms used to earn interest on this. But now the regulators are cracking down on such avenues. Which is a big blow: IIFL Securities for example made a profit of INR 300 Cr in FY22. The interest income earned by IIFL Securities was 180 Crores, this explains how big a blow this can be on the bottom line for these brokers. So profitability could be affected.

But seeing the increased limits on UPI, and the profitability metrics, and the hope that MDR or pricing of some sort comes to UPI (see edition #56 of this newsletter), it’s possible that apart from more UPI Apps focusing on investment as an offering, we see new players entering into the “category specific UPI app” space for investments, or existing UPI Apps pivoting into this:

But what will set these category-specific UPI App for investment apart?

As I mentioned, existing UPI Apps, such as PhonePe and Paytm have launched their products in the broking space: PhonePe with share.market, and Paytm with Paytm Money. However, I’d say that broking specific apps here still have the edge: When I think of trading, or buying stocks or Mutual Funds, a Zerodha, or a Groww (or my respective bank product, such as HDFC Securities comes to mind, not PhonePe)

But keeping aside the PhonePe, and the Paytm product, will newer apps be able to actually differentiate themselves against players who’ve got the distribution within investments? Zerodha, Angel One, Groww have distribution.

The answer seems to lie in specific value propositions, serving a perhaps niche customer base. Take a look at some of the newer investment apps below:

INDMoney, which is coming up, the value prop that differentiates it seems to be US stocks. It’s got ~10M users as of FY24. But it also offering broking for domestic stocks. It’s a UPI App, launched in December ‘24.

Stable Money differentiated on Fixed Deposit Investments, although eventually I do expect it to expand to other products, and eventually get into broking as well. It’s got ~1M users as of FY24. Its getting into government bonds, and a FD backed card. It’s not a UPI App yet.

Curie Money with its innovative “mutual funds on UPI” play: Since the app isn’t live yet, I’m yet to understand the segment it serves, but I’d be keen to try it

Jar: Its value prop is digital gold, but it’s also getting into personal loans. It may eventually do a Zerodha, or a Groww, and get its own NBFC to do loans against securities. It’s got ~20M users has of FY24

All of these apps can serve their purpose without UPI as well. But as I mentioned above, with UPI being such a key part of this experience, and especially as limits are being increased, it makes sense for players in this space to own more of the UPI journey, to be able to innovate faster for their end customers.

What will set these investment apps apart is: how much can the core value prop be differentiated from existing apps.

INDMoney, Stablemoney, Jar, and Curie Money are trying to do this to some extent. While they offer multiple functionalities, the core of what they are known for is different from your standard broking apps. Specificity seems to be the name of the game. This could be either through investments in foreign markets, alt assets such as crypto, start-ups (which players such as Sateeq and Tyke tried to do but failed). Belong is another interesting one: It allows Indians in the UAE to invest money in USD fixed deposits. So niche segments seem to be key for investment apps. And as an investment app: if you’re offering a platform for a customer to purchase something, and you’re funnelling significant volumes through UPI, it’s probably better if you own a piece of the journey

But investment adjacent offerings, where the value is tied to a core value prop of something an existing app has may struggle. Ex: Volt Money offers Loans Against Securities. Groww & Zerodha, with their distribution, and their own NBFCs have a way better right to win here.

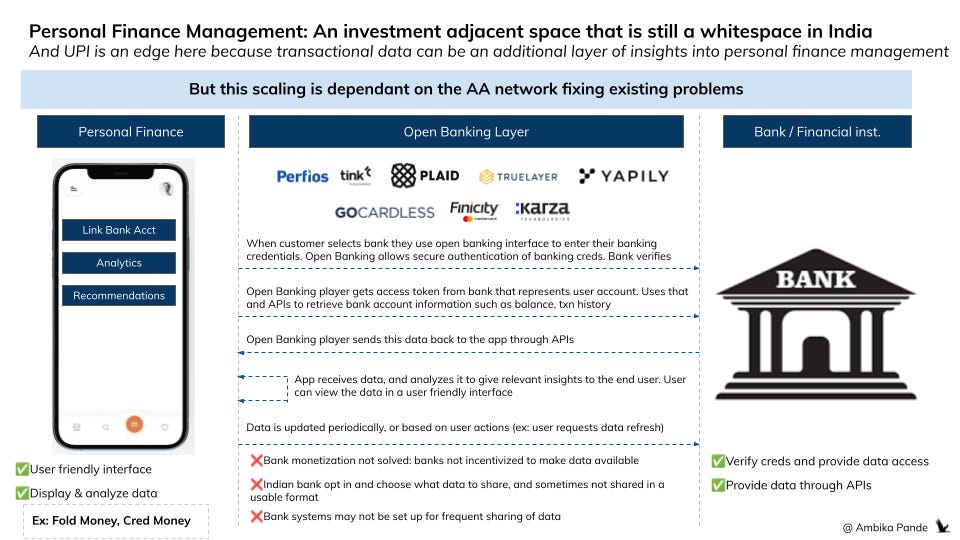

Personal finance management is another opportunity that has not been solved in India just yet, and subject to the AA system scaling, could be an opportunity

This is a key part of investment, so I have included this here. Folks with multiple connected accounts, either through UPI or through tokenized cards have the edge here. I will say though, personal finance management is different from a payments investments app, and this is still a whitespace in India. You can check out Fold Money which is doing some cool stuff here. However, there are issues with India’s Account Aggregator network, but as this evolves, apps that provide better & secure financial management will definitely have a use case.

To check out my piece on the Account Aggregator network, and issues that currently exist with it, see below:

[#44] Open Banking: What's missing in India's Account Aggregator framework?

![[#44] Open Banking: What's missing in India's Account Aggregator framework?](https://substackcdn.com/image/fetch/$s_!GClQ!,w_280,h_280,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fab5b2adf-3720-45b7-9453-e2cd2dc6933e_1750x978.png)

Open Banking is being highly touted as one of the key themes that will evolve in fintech. That, along with CBDCs, and neobanks, are what are being predicted as the key drivers of growth going forward. But what is open banking? I’ve heard folks confuse it with neobanks, core banking systems and basically bank infra.

And as a personal finance management app, if you’re also a UPI App, and are able to facilitate transactions through your platform, then that’s a layer of transactional behaviour that you can use into the personal finance management recommendations. Which then flows into investment / and other purchases.

UPI isn’t really required for personal finance management or investment. But it makes the experience more seamless and increases the value add tenfold. There’s a reason Groww is a UPI App, and Zerodha is on a UPI Plug-in. And why Cred (#5 UPI App) launched Cred Money, a personal finance management tool, and Svalbard in Feb ‘25: which is a mix of personal finance management (predictive analytics, credit score management etc), and LAS (allows credit lines against mutual funds) - though how much of this is value add, and how much of this is marketing, we’re yet to see.

Also: Investment Apps seem to be more efficient from a UPI cost perspective: Higher AoVs, and less # of txns

And there’s another view: UPI transactions have a cost on a per-transaction basis: assumed to be anywhere between INR 0.05 to INR 0.8 per transaction, depending on scale. But investment platforms earn fixed fees (~INR 20) or % commission per trade. And investment platforms have much higher AoVs than the average UPI transaction. On average, the UPI transaction has an AoV of ~INR 1400. Groww, in Jan ‘25, had an AoV of ~INR 7273. INDMoney had an AoV of ~INR 4653. So at least from a # from a transaction perspective, they are pretty efficient. And doing some quick math here: At an AoV of ~7k, a 0.03% commission comes to INR 2. An AoV of ~INR 4653 comes to INR 1.38. So on a per transaction basis at least somewhere costs could be covered.

Groww for example is #17 on the UPI App ranking list in terms of number of transactions but #7 in terms of value processed. So from an efficiency perspective as well, investments as a category for UPI Apps seems favourable.

And hence my view: investments as a category for UPI Apps is going to grow, with existing apps pivoting, and new niche apps coming in

Right now, while the ubiquitous app battle seems to be won, newer apps are going after Credit: Super.Money, with its Credit Focus, the launch of its FD-backed card. Kiwi, with its CC on UPI focus. Navi, with its Credit Lines on UPI partnership with Karnataka bank. But Credit is just another method, and once issued, it can be linked to any UPI app. I’m still on the fence about a separate app winning the credit game, and think it’ll be more around existing scaled apps swooping in when this market scales. And at the end of the day, if your value prop is credit, you still need distribution. Look at global players such as Klarna & Affirm. They started out with their own apps, but now have started partnering with Apple & Google Wallet to show their offering, as a method within the wallet, along with cards, and other fund sources.

To check out my piece on BNPL, you can click below:

![[#42] The Klarna IPO & LazyPay pause: What does the future of BNPL look like?](https://substackcdn.com/image/fetch/$s_!LIzr!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F58fadd95-7f95-4cda-a743-b6996f8f0979_1752x984.png)

But investment is different.

And while I expect newer investment apps coming in, on UPI rails, with a differentiated investment value proposition, I also think that its very possible that out of the 75+ UPI Apps operating, most of the fintech apps shift to investment / personal finance management adjacent offerings as their core product.

|

|